Another day and another fiasco in debt funds. Ever since the IL&FS crisis, debt mutual funds have been going through an intense trial by fire. The number of defaults, downgrades and bust-ups have been astounding. Remember, debt is supposed to be an asset class that’s supposed to provide safety and stability in your portfolio. But what has transpired has been the opposite – equities have been safer than some of the debt funds.

Well, just when you thought things couldn’t get any worse for debt funds, in a stunning and unprecedented move, Franklin India announced that it is shutting down 6 debt funds. Investors cannot redeem their hard-earned money. They’ll have to wait until Franklin figures out a way to sell the papers or they mature. Was this the right move or wrong move? Well, you can debate that until the cows come home and far more brilliant people have written about that.

What basically happened was Santosh Kamath was running a high risk-reward strategy across all his debt funds. His funds had the highest YTMs across categories. For example in October 2018, the month after the IL&FS crisis broke out, the YTM of Franklin Credit Risk Fund was 11.42%, and for comparison, the YTM of ICICI Credit Risk Fund was 10.26%. I’ve compared it with ICICI because the AMC hasn’t had any issues in debt…yet! Even in a relatively safer category like Ultra Short Funds, Franklin’s YTMs were ~1% higher than the competition – it’s was a high-wire act on steroids.

To be fair, at one point, even I was smitten by the returns. Right around the IL&FS or DHFL crisis, I had a one-time income, and I almost invested it in Franklin Ultra Short Fund, but better sense prevailed. I’m not ashamed to admit that the sole reason I chose the fund was the returns and the popularity.

Look at the returns of Franklin funds, those are equity-like returns. It was nothing short of incredulous when the going was good.

And this inevitably showed up in the AUM. Here’s the AUM growth of the 6 schemes that are being shut down since Jan 2016. Even post the IL&FS crisis (shaded region) when there was risk aversion in debt funds, the AUM continued to grow.

The easiest thing to say with the enormous privilege of hindsight is that these things generally have a bad ending. Things have been bad for FT debt schemes since 2019 when people started having worries over risky credit exposure. It seems like the Vodafone episode coupled with COVID-19 was the tipping point, and the redemptions increased.

When a mutual fund gets more redemptions than purchases, it usually sells the bonds that are easier to sell first. As things get worse, it’s left with the less liquid and hard to get rid of papers and this is what has happened in FTs case. It tried selling papers, borrowed money to pay redemptions, and finally, it seems like shutting down the schemes was the only poison pill left.

This whole thing reminds me of one of my favorite quotes:

More money has been lost reaching for yield than at the point of a gun.

Raymond DeVoe Jr

Who’s to blame?

Well, there’s a lot of blame to go around here. Santosh Kamath has been pilloried, but I’m going to take a slightly different view here. Does he deserve the blame? Of course. He ran a high risk, high reward strategy by lending to riskier companies. In a normal market environment, who knows, he could’ve pulled maybe pulled this off for longer. But liquidity is a fickle mistress! But does he deserve all the blame? Hell no!

The advisors (IFAs/RIAs), distributors, platforms, dumbass retail investors, everybody are to blame.

What’s the point of paying ~1% to a distributors/advisors who don’t even have the ability to distinguish risk in debt, forget equity! And make no mistake, Franklin distributors were handsomely compensated for distributing these funds! Investors meanwhile were blinded by those delicious almost doubt digit returns. And platforms, well, pretty much all of the top platforms were recommending these schemes.

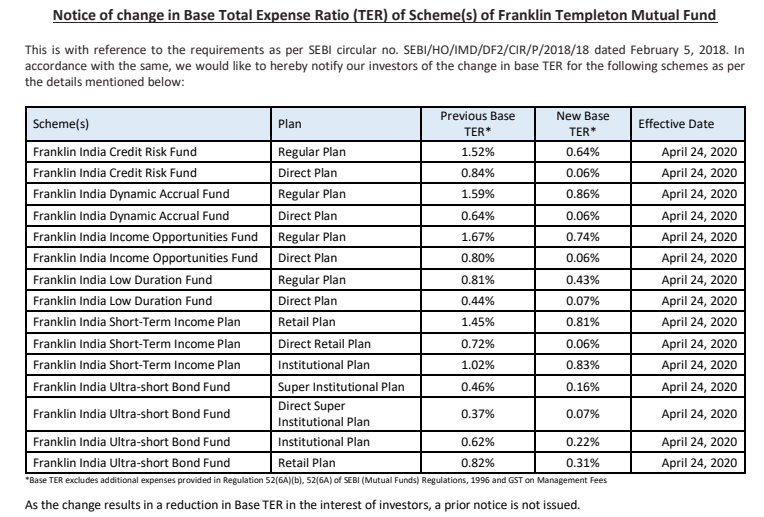

What happened post the event is even stunning. Franklin slashed the expense ratios of the direct plans of these funds but not regular. Does it mean that distributors will continue to get paid for the brilliant job they have done? I’m not yet sure.

This whole sordid episode is yet another crash course in investors penchant of doing the same dumb shit over and over again.

Curve flattened!

Beyond Franklin

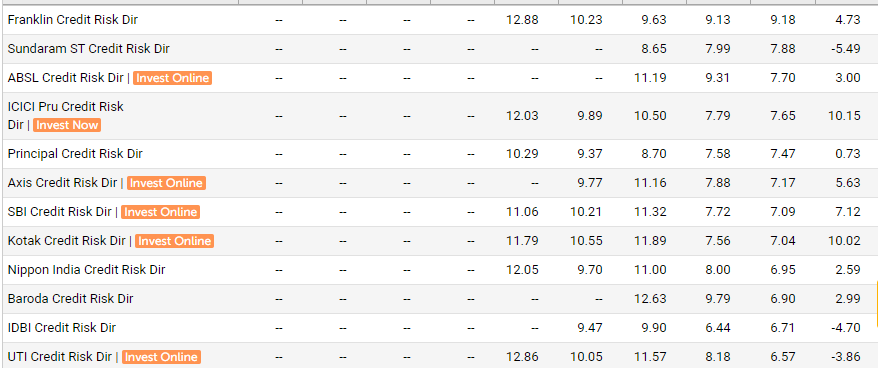

Franklin’s strategy was like driving at 150 km/h without airbags, crashing and burning, that I understand. But other larger AMCs like UTI, Nippon, and ABSL must be ashamed of themselves because they were driving at 40 with airbags and still managed to have a frontal collision with cars that were parked. They have messed up spectacularly and hilariously trying to keep up with FDs let alone beat them, and I am aware of the ironic comparison here.

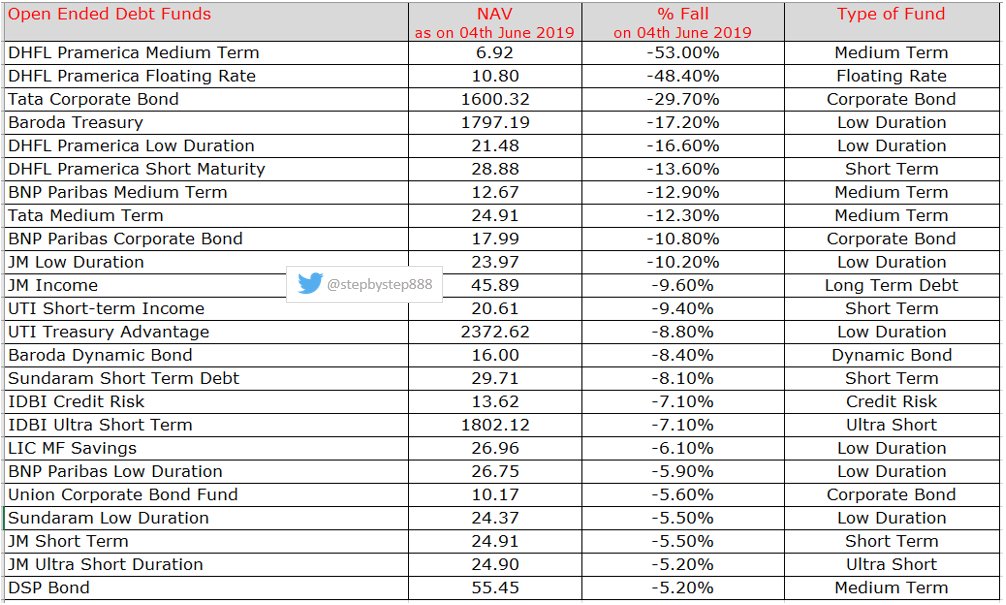

Look at the expense ratios of these funds, they are almost on par with equity funds. Is this what people are paying for this garbage process and philosophy? Here’s how some of the funds fared post the DHFL default. To be fair, most of the money in the DHFL schemes had fled and they were just left with their own papers with about 100-200 cr AUM. But the others, it’s unconscionable.

Again, all of this was happening in an asset class that’s meant to be safe. Irony died a million deaths! Before you think “everything has risk”, there were plenty of large AMCs which managed to come out unscathed since the IL&FS crisis broke out such as SBI, ICICI, Canara, IDFC etc. How the hell did they manage?

#DebtMutualFundsAwesomeHai

For all the talk about doing right by the investors, the Indian mutual fund industry as a whole must be ashamed of itself when it comes to how it has handled debt. If I am paying a supposed all-knowing superstar to manage my money who doesn’t even have the ability to avoid obvious landmines like DHFL, IL&FS, Reliance ADAG etc, what’s the use of these fund managers? A monkey could have avoided these papers!

And not to mention the risks in hybrid funds and FOFs. Because right now Dynamic Asset Allocation/Balanced Advantage Funds (mis-labelling) and Hybrid Funds are the flavor of the season. With Nifty down 2% YTD, AMCs are hawking these funds as having fallen lesser than 100% equity. Of course, some funds have done well, no doubt but there are skeleton there too. Nippon and ABSL’s hybrid funds have had issues. Again, the Indian mutual fund industry should be ashamed. These funds have long been mis-sold in varying forms from compulsory dividend plans to safer alternatives to equities and FDs. But, these AMCs have managed to mess this up too.

Given the mess in the debt funds, Franklin India decided to mark don the debt exposure in it’s hybrid funds considering their illiquidy. Luckily, expect fro the Dynamic Allocation FOF with the AUM of Rs 878 crores, the other funds are in low single to double digits in AUM.

It’s just been a series of disasters. And I am pretty sure nothing is going to change. In a few months, investors will forget this whole sordid mess, go back to doing the same silly things they did before. And the fund managers will again resort to the same shenanigans they did before to extract that 1% extra yield to get a 5-star rating or a bonus and distributors will start hawking some new shiny fund.

Speaking of star ratings when will the likes of Value Research Morningstar wake up to their flawed methodologies and when will they start cautioning investors actively? These ratings have caused more harm to investors than the sum of all mis-selling by bank relationship managers.

If anybody here is under an assumption that things are going to change post-Franklin – let me assure you, they won’t! Never underestimate investor inertia, greed, and stupidity!

The rent seeking must continue at all costs!

Perhaps the greatest gift you can give your loved ones is to protect them from the traditional securities industry, which has a long history of transferring wealth from their clients to themselves.

Dan Solin

In spite of all the supposed “evolution” (don’t know WTF that means) of the Indian mutual fund industry we still don’t have decent 0 credit risk funds. We just have long duration GILT funds which are too volatile for most retail investors. There are no T-bill only funds, there are no short and intermediate G-Sec funds. These products, if they existed, would be all investors needed. Hell, if these funds could be sold as wrappers, that would be best for retailers.

Now, the luminaries

I’d be remiss if I didn’t talk about the stars of the show – the dumbass retail investors. Every time the markets crash, people from the industry come out, point toward the stable SIP flows and say “retail investors have finally matured”. This has to be the biggest joke if you ask me. There are no absolutes. Yes, some people will learn and make better choices. But at any given point of time, the number of idiotic retail investors far outweigh the number of sensible ones.

There will always be a sizable chunk of retail investors who can never be saved. These people will chase shiny objects, past performance, high returns, star ratings, senseless recommendations by talking heads, AMCs, friends etc and light their hard-earned savings on fire.

One prime example is the credit risk funds category. I’ve been wracking my brain to figure out one reason to invest in this stupid category of funds, and I can’t seem to come up with one. I’ll also concede that I have the IQ of a dried coconut shell lying on a street, but still.

Do you really need a debt fund?

Post the SEBI rationalization of mutual fund categories, there are 16 categories of debt funds. You could argue all day if this categorization exercise made life easier or harder for investors. But that aside, apart for about 6-8 categories such as overnight, liquid, ultra-short, money market, banking and PSU, corporate bond, and maybe gilt in some cases, I cannot think of a single reason for investors to chose other categories like credit risk, dynamic bonds, mid to long-duration funds etc.

Most retail investors just chase returns in debt funds. For ex, gilt funds are all the rage now given the series of rate cuts they have delivered double-digit returns in the last couple of years. But if the situation turns around and there are rate hikes, these people will flee these funds. Moreover, for a good chunk of people, debt funds are a puzzle. They refuse to understand duration risk, interest risk, and credit risk. It’s not easy, there’s a learning curve, which the dumbass retail investor doesn’t want to go through. Star ratings are easier, and this has been suicidal. Most of these funds which have blown up had 4-5 stars at some point or the other.

The thing is some investors might not even need debt exposure given that most would be investing in EPF, PPF etc. Add to that, Indians traditionally have a lot of scammy insurance policies meaning most retail investors are overexposed to debt. They refuse to understand the simple concept that debt is meant to preserve money or at the most grow slightly more than inflation while equity is meant to do the job of delivering returns.

I hope retail investors don’t continue to do dumb things over and over again, never learning and expecting a different outcome. But I have full faith that they won’t!

Indexheads India Newsletter

A newsletter on indexing and sensible investing.

Dont forget that u too are one of the dumbass retail investors.Also IlFS and DHFL fiasco came as surprise and don’t forget both were rated as AAA. Also best of bests didn’t hv any clue when DHFL share fell from 610 to 250 in a day and everyone were searching for an answer to knw what had happened.

Every bad investment looks as landmine only in the hindsight!!

I have been researching debt funds for a few months and it is more confusing than informative as I read more. My problem is unique in the sense that I am overexposed to equity from the start of my career and am on the look out for options that would balance the equity risk in the next couple of years. I am alright with taking a bit of reinvestment risk and/or a bit of credit risk. I do not want to go the route of FD because interests get taxed at high end of the tax slab. I am surprised there are no simpler products available in the market like index funds for debt. Any recommendations for someone like me?

I am also looking for same.go to freefincal.com and download the free e-book how yo invest in debt mutual funds.Stick only to liquid and ultrashort term funds. learn terms like yield to maturity and modified duration before you invest.

Anand, my standard response whenever someone asks me a similar question is:

“I am not qualified to give you advice. The best way to fuck up your portfolio is to take random advice from idiots like me. Learn and DIY or hire an advisor. I know this isn’t the answer you were expecting. But in 10-years you’ll thank me”

But these posts are a good place to start in understanding all the categories and figuring things out: https://freefincal.com/debt-mutual-fund-categories-explained/

https://www.primeinvestor.in/how-to-identify-risks-in-debt-funds/

oops, should have been more clear. I was not looking for specific advice, I was looking for direction on the category like “index funds for debt” kinda thing more than a specific fund recommendation! Freefincal has been the backbone of all my research and stupid mistakes on my portfolio are proudly my own, not that of some random idiot on twitter! 🙂

Bharat Bond ETFs/FOFs are the only pure index debt products. There are constant duration Gilts too, but incredibly risky. Apart from that, these are still very early days for debt index products.

Bharat Bond ETFs/FOFs are the only pure index debt products. There are constant duration Gilts too, but incredibly risky. Apart from that, these are still very early days for debt index products.