The best way through bullshit was to wade in, hold your nose with one hand and a grenade in the other, and cut straight to it.

Alexandra Bracken

In the past couple of decades, there have been several megatrends in asset management like the rise of index funds, target-date funds, thematic funds, smart-beta funds 🤮, ETFs, and so on. Each of these megatrends have resulted in billion to trillion-dollar shifts and have fundamentally altered the asset management landscape globally. The latest trend that looks like it is shaping up to be a megatrend is environmental, social, and governance (ESG) investing.

This post is an exploration of what ESG is and the implications for you as an investor and also on the markets.

What ESG?

Why ESG?

How ESG?

Should companies focus on ESG?

Does ESG mean higher returns?

90% of mainstream ESG is bullshit!

Peeking under the hood of ESG funds

ESG is just active management in a new lungi!

Are you making a difference?

The mother of all ironies

50 shades of ESG

ESG in India

ESG and fiduciary duty

Ok, so ESG is useless then?

Goddamnit! Is there no way I can make a difference with my investments?

Everything will be ESG

The biggest megatrend

Parting thoughts

Every investment survey of late shows ESG as the top consideration among investors and asset managers. Millennials apparently, seem to be hellbent on investing in ESG funds and save the world. If you go by the reported numbers, there’s anywhere between $1 to $60 trillion of assets in these funds broadly defined as sustainable strategies.

Asset managers globally have been on an ESG fund launching spree. ESG consultants have sprung up like mushrooms after a rainy day. Everybody from company CEOs, financial advisors, central banks to my maid now wants to be ESG compliant. Companies, asset managers, pensions, wealth funds are becoming signatories of organizations that promote “sustainable investing practices” and are making pledges to cut carbon, oil, bring about gender equality, and waterboard CEOs and directors to do good. It’s a sustainable war!

I’m going to get skewered and probably be murdered in an eco-friendly way by the true believers for expressing scepticism but here goes. I think the hype about ESG investing far outweighs the reality. While people like Jared Dillian have called it a bubble, others like Chamath have even called it an outright fraud, but take that with half a bucket of salt.

Perhaps the worst thing that has happened is that the Wall Street and Dalal Street machine has co-opted ESG and is milking it for all it’s worth. As Ben Hunt says, “They’re Not Even Pretending Anymore”..

I like keeping track of all the shenanigans in the asset management industry, and I’m amazed at what asset managers are doing in the name of ESG. Initially, I didn’t think much of ESG and assumed that it must be just another trend because I knew very little. But over the past few years, as the noise about ESG got louder, shrill even, I became curious and started trying to figure out more. But the more I learned about the mainstream version of ESG peddled by large asset managers, the more depressing it got. The blatant hypocrisy, lies, doublespeak, and deceptive narratives are just scary, and I think investors will end up paying the price.

So this is my earnest attempt to think through this mess as I write this post, and hopefully, you might find it useful too.

What ESG?

Before you even know what the acronym ESG stands for, I think it’s important to understand the definition of ESG lies in the eyes of the beholder. If you ask 23 people about what ESG means, you’ll get 69 answers. There is no one true definition.

But we still gotta know what we are talking about. The acronym ESG stands for environmental, social, and corporate governance. ESG investing is the consideration of environmental, social, and corporate governance factors when investing.

Example of some of the 100s and 1000s of factors that can be considered from an ESG lens.

Show me your ESG, and I’ll show you mine

Given that there are no universally accepted definitions of ESG, how you define ESG might be vastly different than how I would. Which means ESG is quite personal. The E, S, and G issues that might matter to you are a reflection of your values system and are unique to you. While you might think climate change is the most pressing issue, to me, gun control and gender diversity issues might matter more. There’s no right or wrong here; it’s just that people are complex and have different priorities.

In summary, ESG Is an amorphous term, it can mean a whole lot and very little at the same time.

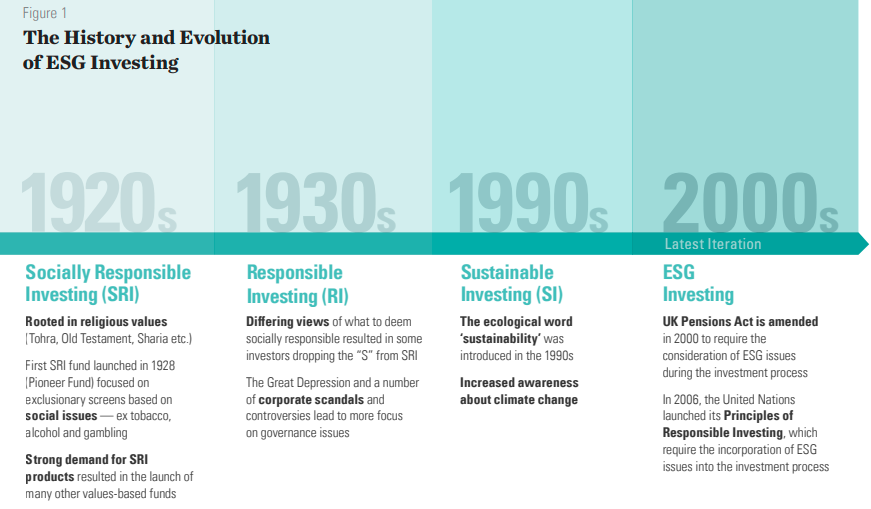

ESG isn’t new, it’s just the latest avatar in a long evolution spanning a century.

ESG advocates view ESG as being directly in conflict with the famous Milton Friedman doctrine of a company’s purpose.

Corporations have no higher purpose than maximizing profits for their shareholders

Milton Friedman

But as Professor Aswath Damodaran, who is called the dean of valuations, writes, what Milton Friedman says and what ESG proponents want maybe the same thing, if looked closely.

Much of the ESG literature starts with an almost perfunctory dismissal of Milton Friedman’s thesis that companies should focus on delivering profits and value to their shareholders, rather than play the role of social policy makers. The more that I examine the arguments that advocates for ESG make for why companies should expand mission statements, and the evidence that they offer for the proposition, the more I am inclined to side with Friedman. After all, if ESG proponents are right, and being good makes companies more profitable and valuable, they are on the same page as Friedman. If, on the other hand, adopting ESG practices makes companies less valuable, the onus is on ESG’s proponents to show that societal benefits exceed that lost value.

Aswath Damodaran

ESG is largely non-financial in nature, and the definitions can be extremely fuzzy. Unlike traditional metrics on which stocks are evaluated and chosen, it’s hard to attach a rupee value to ESG parameters. Some people like Fiona Reynolds, the CEO of United Nations Principles for Responsible Investment (UNPRI) argue that the acronym ESG itself is pointless and pigeonholing issues into these 3 buckets does more harm than good, and I agree with her. ESG is a stupid and pointless label, and I’ll explain why as you brave this torture with me. At this point, I’d like to apologize for putting you through this torturous exploration of ESG.

Now, these are still early days for ESG investing, and it’s the wild west. There are no accepted definitions, frameworks, or reporting standards among ESG data providers. ESG today is what you want it to be. And this vacuum has led to rampant greenwashing, i.e. slapping a green label on products to claim they are ESG compliant.

Why ESG?

Most people say that the popularity of ESG is because this world is going to hell in a handbasket because of climate change, the Me Too movement, increasing scrutiny of governance practices of companies, the rise of the conscientious millennials, enlightenment among asset managers that they must do good as well and so on. Sure, all valid reasons. But without the internet and ad-supported media, ESG wouldn’t have been as big a trend.

To me, it is always astounding how much we take these two things for granted. Investors, fund managers have always implemented some version of ESG in their investment processes without having an explicit label. After all, who wants to invest in “bad” companies? It’s just that there is now a label, and it’s a trend. And if you extend this line of thought, ESG is somewhat meaningless because it has always been a part of the investors’ processes in some shape or form.

But I don’t want to piss off the green warriors by continuing with this line of thought anymore. I’ve seen movies where green fanatics have killed and bombed people for less💣 My bucket list is still quite unfinished. I’m yet to take Prashant Jain’s autograph on a printed factsheet of HDFC Top 100 Fund, get high and read The Intelligent Investor, watch RGV Ki Aag, among other things.

The bottom line is that like it or hate it, ESG is here to stay, and it’s a monstrous mega trend in asset management. Mark my words, ESG as a trend will dwarf index investing. For scale and context, index investing resulted in over a $2-3 trillion shift in investing dollars in the US. ESG will probably be 5-50X of that.

How ESG?

Negative screening: One of the most common approaches to ESG is negative screening, although the application of this approach is reducing. This involves excluding certain sectors or categories of stocks based on a set criterion or a values system. For example, screening sin stocks (drugs, gambling, alcohol, prostitution). According to various estimates, a huge chunk of sustainable assets follow this strategy.

Best-in-class or positive screening: In this approach, instead of screening out stocks, they are ranked based on ESG data, most commonly ESG scores. A portfolio is then constructed that is overweight stocks with the best ESG scores and underweight stocks with weaker ESG scores.

ESG indexing: Perhaps, the most common approach in vogue today. These funds and ETFs track ESG indices constructed by index providers like MSCI, S&P, NSE, Morningstar etc. These funds have become the easiest way for both institutions and retail investors to allocate to ESG.

ESG integration: This is a more holistic approach in which material ESG factors are considered along with traditional financial analysis and valuation approaches.

Thematic strategies: These strategies target a particular ESG factor. For example, clean energy funds, low carbon funds, gender diversity funds etc. Off late, some of these funds have gained quite a bit of traction among individual investors.

Active ownership: This is similar to activist investing. An asset manager builds a meaningful stake, obtains board seats and tries to influence a company’s approach to ESG issues through voting and continued engagement.

Impact investing: These tend to be specific investments made to target a particular outcome — for example, clean water projects, schools in rural areas, affordable housing, etc.

Should companies focus on ESG?

This question strikes at the heart of the purpose of a company. Is the duty of a company towards its shareholders or stakeholders? Milton Friedman famously wrote:

There is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception fraud.”

A Friedman doctrine‐- The Social Responsibility Of Business Is to Increase Its Profits – The New York Times (nytimes.com)

This view, also known as the Friedman doctrine, has become the bedrock of modern capitalism. On the other hand, the stakeholder theory proposed by Edward Freeman says that a corporation shouldn’t just focus on maximising its profits but should also focus on the interests of its stakeholders like its employees, suppliers, the government and other parties that are impacted by its operations even if it means lesser profits.

The shareholders vs stakeholders debate is one of the longest-running debates in corporate finance. As I was writing this post, I was tempted to settle it once and for all, but I have some pending shows to catch up on Netflix, so I’ll settle this later.

Look, there are multiple competing views here. People who support the Friedman view take pains to point out that his doctrine says that a corporation has to operate without deception or fraud. And that this is as good as saying a company has to be considerate towards the broader stakeholders. The proponents of the stakeholder capitalism theory say that modern enterprises are running amok and are destroying the planet to maximise their profits without worrying about the societal or environmental impact. And then some people are of the view that both views can co-exist.

As with all debates, there’s no single answer here. Things in the real world are infinitely complicated, and a company cannot behave in just one way. Look, I’m nowhere near qualified to have a view on this issue. But it’s important to know this because If you look at the marketing of ESG funds, they are often sold as good for everyone. Good for the companies, investors, stakeholders, the planet, galaxy and god himself.

They say if it’s too good to be true, it usually is….. Unless it’s me.

Behdad Sami

ESG marketing would have you believe that you can have your cake and eat it too. I wonder where I’ve heard that before? Oh, wait, every scam, fraud, dud, pointless investing solution ever!

But let’s unpack this. Should companies focus on ESG issues? Most people will agree that companies should care about the environment, society and should have the highest governance standards. On the other hand, the people who conform to the Milton Friedman view that that the sole responsibility of a company is to maximize shareholder profits. These people might argue that ESG issues are just a costly distraction for the companies.

Now, the asset managers and consultants will tell you, citing spurious and incomplete research, that ESG friendly companies are always profitable. But here’s the problem with such sweeping statements, every choice that a company makes or focuses on has a cost, and every choice has a trade-off. As a small thought exercise, consider this example from this MIT Sloan article on the shareholder vs stakeholder debate. Assume a company has a chance to save costs and increase profits by outsourcing its manufacturing overseas. The shareholder primacy theory would support it. But the stakeholder theory would expect the manager of the company to spend on retraining employees and think about the impact of the community at large than just focussing on profits and moving the operations overseas.

There are several trade-offs here, and things are never cut and dry. This is just a small example to give you an idea of how complicated and nuanced these questions are.

Everybody agrees that companies shouldn’t destroy the planet, pay their employees fairly and not commit fraud. But all these actions come with costs and trade-offs that can impact profitability either positively or negatively. These choices also have an impact on the shareholders of the company. Not just the owners but common people who’ll be holdings these stocks in their retirement accounts and so on. Making blanket assertions that ESG = higher profitability = higher returns will only damage the credibility of ESG as a philosophy.

Here’s a rather relevant excerpt from the father of modern finance, Eugene Fama’s recent working paper:

On the asset pricing side, what are the costs and benefits to firms in choosing products and production techniques oriented toward E&S goals. If some investors value the E&S actions of firms, then given net cashflows, E&S virtue by a firm is rewarded via higher share prices, which imply lower expected stock returns and costs of capital. Lower costs of capital help firms in the competition for survival. But adopting E&S goals is also likely to raise production costs, which leans against the benefit of lower costs of capital. Lower costs of capital for E&S accredited firms also mean that for E&S investors, virtue is its own reward since investors get lower expected returns from the shares of virtuous firms. This is the bottom line from most of the work on this topic, including Fama and French (2007) and Pastor, Stambaugh, and Taylor (2020). Needless to say, lower expected returns are not prominent in the marketing materials of ESG money managers.

Professor Damodaran, in his exploration of ESG, comes to the following conclusion:

In summary, based upon the studies so far, the strongest evidence in support of ESG seems to be that “bad” companies face higher funding costs (from debt and equity), whereas the evidence on ESG paying off as higher profits and growth is elusive. There is some evidence supporting the proposition that being socially responsible (or at least not being socially irresponsible) can protect companies from damaging disasters, but selection bias is a problem.

From whatever I have looked at, I’ve pretty much found the same. I’ve seen studies that show companies that focus on ESG issues can deliver abnormal alpha, and I’ve also seen studies that ESG does very little to enhance profitability. But in my mind, both these studies suffer from the same faults, i.e. poor data. Like I mentioned at the beginning of the post if companies up until recently didn’t make ESG disclosures, and at best, made only voluntary disclosures which would’ve been biased, how valid are the studies based on such data?

There have been several studies that have found issues with ESG datasets used in studies too. Given all this, I’m calling bullshit on the claim that ESG = high profitability. The answer to this question is far more nuanced. Don’t get me wrong, some ESG issues might add to a company’s profitability, and some might subtract it. It really depends on what you are looking at. Remember, E, S and G are three distinctive issues with no commonly accepted definitions and measurement standards.

Professor Fama again:

E&S (environmental and social) issues are more complicated. If environmental and social goals enter consumer utility functions, they provide incentives for firms to provide products that accommodate these goals. For example, if many consumers prefer the more expensive to produce meat of free-range chickens and cows to the meat of their caged brethren, firms will provide free-range meat without Government incentives. Consumers vote via their purchase decisions, and value maximizing firms produce the right amount of more expensive free-range meat. In this way, markets provide solutions to some E&S problems.

In the same paper, he also says, asset markets are also part of the solution.

In a bit to tap into the growing demand for ESG, consultants like McKinsey have published all sorts of nonsense claiming that ESG friendly companies deliver buckets and buckets of alpha (outperformance). McKinsey preaching about ESG is a bit like Donald Trump talking about ethics and honesty. Here’s just how ESG friendly McKinsey is:

Though McKinsey has not been charged by the federal government or sued, it began to worry about legal repercussions in 2018, according to the documents. After Massachusetts filed a lawsuit against Purdue, Martin Elling, a leader for McKinsey’s North American pharmaceutical practice, wrote to another senior partner, Arnab Ghatak: “It probably makes sense to have a quick conversation with the risk committee to see if we should be doing anything” other than “eliminating all our documents and emails. Suspect not but as things get tougher there someone might turn to us.”

McKinsey Proposed Paying Pharmacy Companies Rebates for OxyContin Overdoses

Not just this, McKinsey was involved in the now-infamous mega state capture scandal in South Africa too. It was actively complicit in helping the Guptas, an Indian origin family, to steal billions of dollars of government money.

As Charlie Munger said:

Show me the incentive and I will show you the outcome

The incentive for everyone peddling some variant of ESG is a fat cheque. Nothing wrong with it, but not when the practices are dishonest, and I’ll get into more detail about just how shady and unethical the practices of some of the biggest proponents of ESG are apart from the McKinsey example above.

To sum up, my issue has been with the duplicitous ESG sales pitches that all things ESG are good for the investors. There’s no conclusive evidence of that yet. We might one day but not yet. Whether companies focus on ESG issues isn’t solely their choice. Companies answer to shareholders. The answer to this question also depends on regulations, consumers, asset managers, advocacy groups, lobbyists and so on.

Asset managers on their own aren’t the sole deciders of a company’s focus. And this gets even trickier as we go along. Who are asset managers to decide what a company should do? Shouldn’t they be working to maximise the returns of the investors whose money they are managing? Sure, they say that ESG is good for returns hence their push to drive companies to do good. But what if it doesn’t end there? What if an asset manager decides to project his morality, his subjective views of what’s right and what’s wrong and tries to express those views through other people’s money he is managing? After all, we all know just how ethical asset managers are.

The answer, as will most things in life, is context-dependent. There are no blanket answers.

Does ESG mean higher returns?

By now, if you have appreciated the sheer vagueness and fuzziness of what ESG means, you’ll know that the answer to this question is incredibly complicated, to say the least. But, at the end of the day, you have to appreciate the fact that not all ESG investors are bleeding-heart do-gooders. People might signal all sorts of virtues, but a good chunk of people only care only about returns at the end of the day. Whether rightly or wrongly is again a matter of perspective, as all things ESG are.

All things said and done, we can’t avoid this question. But the answers are, again, tricky, to say the least, so I’ll try to unpack this.

To answer whether ESG = higher returns, again, it pays to be specific about what version of ESG we are talking about. Because like I said, most people write and talk about ESG as if there’s just one version of ESG, which isn’t the case. Let’s start with any ESG strategy that screens out certain stocks or excludes them, a negative screening strategy.

Now, most of the ESG funds available for retail investors will exclude sin stocks like tobacco, alcohol, gambling, adult entertainment and certain weapons manufacturers. This is what you call a constrained strategy, given the limitations. Now, if an ESG fund has a constraint while a traditional fund doesn’t, how can asset managers claim that a constrained strategy can deliver outperformance over an unconstrained one? This is exactly what Cliff Asness, the founder of factor investing giant AQR, wrote in perhaps one of the most important pieces ever written on the topic of ESG:

Put simply, if two investors approach an asset manager, one who says “just maximize my return for the risk taken” and the other who says “do that but subject to the following constraints,” it is simply false and irresponsible for the asset manager to assert that the second investor should expect to do as well as the first, except in the case where those constraints are non-binding (and therefore not relevant). Even in that case, it’s still irresponsible to say that the second investor should expect to do better.

Frankly, it sucks that the virtuous have to accept a lower expected return to do good, and perhaps sucks even more that they have to accept the sinful getting a higher one.17,18 Well, embrace the suck as without it there is no effect on the world, no good deed done at all. Perhaps this necessary sacrifice is why it’s called “virtue.”

Virtue Is its Own Reward: Or, One Man’s Ceiling Is Another Man’s Floor

Even Professor Damodaran shares the same view:

To begin with, the notion that adding an ESG constraint to investing increases expected returns is counter intuitive. After all, a constrained optimum can, at best, match an unconstrained one, and most of the time, the constraint will create a cost.

Sounding good or Doing good? A Skeptical Look at ESG

That’s the returns side of exclusions. But excluding stocks has trade-offs. The sales pitches that you are doing good by excluding companies is just nonsense. Assuming that a tobacco company has poor governance practices, the right way to bring about change is not by removing it from a portfolio but rather owning it and engaging with the management to bring about change.

Moreover, there is a second-order effect to screening stocks. All stocks have to owned by someone. If you don’t own sin stock, someone has to, and why will someone own a sin stock? Because they get paid to. By not owning stocks, the prices of the excluded stocks have to fall. And at some point, they become attractive enough for someone to step in buy them, AKA value investing. Since these stocks would’ve become cheap relative to their fundamentals, they’ll now have a higher expected return. Of course, not all cheap stocks due to ESG screening are good investments. If only it were that simple, you could build an anti ESG portfolio and make some serious money. Some of these stocks may also end becoming value traps, as both Shyam and Klement point out:

Cliff Asness again:

What happens when one group of investors, call them the virtuous, simply won’t own a segment of the market (the sin stocks)? Well, in economist terms the market still has to “clear.” In English, everything still gets owned by someone. So, clearly the group without such qualms, call them the sinners, have to own more than they otherwise would of the sin stocks. How does a market get anyone, perhaps particularly a sinner, to own more of something? Well it pays them! In this case through a higher expected return on the segment in question. This may be unpleasant but it is just math (like math could ever be unpleasant). In the absence of extra expected return the sinners would own X of the market segment in question. The only way to get them to own X+Y is to pay them something more. Now, assuming nothing else changed, how does the market assign this sinful segment a higher expected return? Well by according it a lower price. That is, if the virtuous decide they won’t own something, the sinners then have to, and they have to be induced to through getting a higher expected return than otherwise. This in turn is achieved through a lower than otherwise price

Virtue Is its Own Reward: Or, One Man’s Ceiling Is Another Man’s Floor

George Serafeim, one of the biggest names in the sustainable investing space, also shares a similar view and extends it further on the perverse outcomes of screening and divesting:

Markets have a fundamental correction mechanism for when a company’s valuation falls significantly below its cash flow generating capacity: at some point a buyer steps in, often from private markets. Private equity funds do this best, buying up cash rich companies that are undervalued by public markets. Were divestment ever to succeed in lowering the valuations of fossil fuel companies, an unintended consequence could be a shift from public markets to private markets, if carbon tax regulations are not enforced fast enough. Such a shift could hurt transparency; companies that go private have minimal reporting obligations and they typically become very opaque.

Divestment Alone Won’t Beat Climate Change

Exclusion is highly subjective and nuanced.

So that’s about the question of whether screening strategies lead to good or bad performance. What about other strategies?

Ok, here’s how I think about this

90% of mainstream ESG is bullshit!

Before you even look at the mainstream ESG funds, it’s important to look at the motivation of these asset managers to launch sustainable investing products. It always pays to look at the incentives if you want to figure out why someone is doing something.

ESG investing, in my view, is less about millennials wanting to change the world than Institutional investors like sovereign wealth funds, pensions, hedge funds coming under increasing pressure to “do good” with the money they manage. The easiest way for these institutions to do that was to window dress their investments by screening existing holdings based on ESG scores and tilting toward companies with high ESG scores. Or just buying an ESG ETF and adding it to their portfolios.

ESG, up until recently, was predominantly a European trend. Unlike the Americans, Europeans tend to be a little more conscientious and care about E, S, and G issues.

Doing good has rarely mattered as much as sounding good. And sounding good is way easier than doing good. And where there is demand, there’s supply, and asset managers are just catering to this demand by launching sustainable products.

And then, on the other hand, there has been an incredible cost compression across all swathes of the financial services industry. Post-2008, expense ratios on active funds have fallen sharply thanks to the rising popularity of low-cost index funds.

ESG is just a new shiny mousetrap for most asset managers to charge more than actively managed funds. It’s a question of margins rather than “doing good”, whatever that means.

If you’re one of those “be positive” types, you might ignore this as being excessively cynical. But the asset management industry didn’t retain its 30-40% margins by doing the right things, and I’ll explain we go along.

Ratings charade

To understand the sheer mockery of what passes for an ESG fund these days, you’ll have to understand how these funds are constructed. Pretty much all ESG funds are based on ESG ratings. And the thing about ESG ratings is that they are a joke.

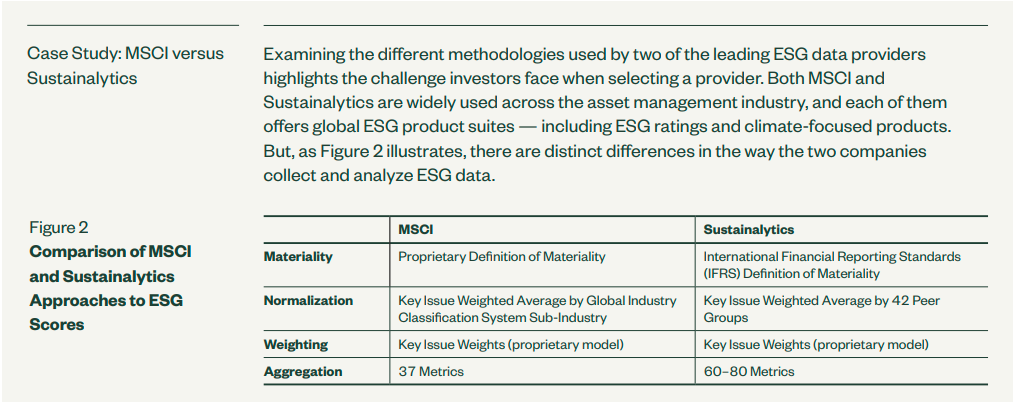

There are 100s of firms like MSCI, Sustainalytics owned by Morningstar, Bloomberg, Refinitiv (Thomson Reuters), and S&P who sell ESG ratings and data. An ESG score or a rating is a single aggregated data point that shows how good or bad a company is on ESG issues. Each of these companies have their own proprietary methodologies to analyse and rate companies globally. Here’s a comparison of the methodologies of MSCI and Sustainalytics by State Street.

Here’s the problem with these ratings or rankings. To begin with, as I mentioned at the beginning, there is no definition of ESG. It’s personal, and it’s whatever you want it to be. Add to that, most companies don’t yet make ESG disclosures or worse yet, make half baked or voluntary disclosures. These disclosures are not just biased but are meant for corporate window dressing. Regulations governing ESG disclosures are still in their very early days globally.

So all these ESG data providers rely on public disclosures, scraping company disclosures, scraping news articles, social media, data published by NGOs, govts, surveys of companies, 3rd party data sets, among others, to make ESG judgements. You see where I am going with this, right? This is fraught with so many issues and problems, and I don’t know where to begin.

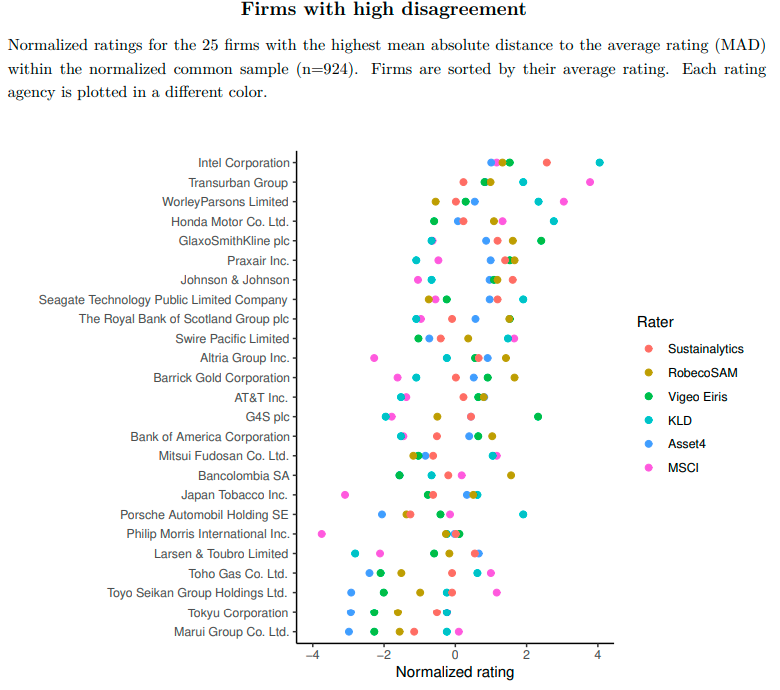

Given this, there is an insane divergence in ESG scores or rankings of the same company across different ESG data providers. Florian Berg, Julian F. Koelbel, and Roberto Rigobon of MIT Sloan analysed this divergence. The results are shocking and funny to me personally, given my deep-seated cynicism of mainstream ESG.

Here are some firms with the highest divergence in ESG ratings they found in their study. That’s scary!

This is a result of a very amorphous definition of what ESG can be.

The research team — Florian Berg, Julian Koelbel, and Roberto Rigobon, all associated with MIT Sloan’s Sustainability Initiative — found the correlation among those agencies’ ESG ratings was on average 0.61; by comparison, credit ratings from Moody’s and Standard & Poor’s are correlated at 0.99. That means “the information the decision-makers receive from [ESG] ratings agencies is relatively noisy,” the paper states — a condition researchers call “aggregate confusion.”

Aggregate Confusion: The Divergence of ESG Ratings by Florian Berg, Julian F Kölbel, Roberto Rigobon :: SSRN

The divergence in the ESG rankings or scores can have far-reaching implications on investment allocations, policy, to ESG research. Many ESG researchers use these ESG data sets, and their conclusions can vary quite starkly depending on which data provider they use.

Therefore, even if a large fraction of investors have a preference for ESG performance, the divergence of the ratings disperses the effect of these preferences on asset prices. Second, the divergence hampers the ambition of companies to improve their ESG performance, because they receive mixed signals from rating agencies about which actions are expected and will be valued by the market. Third, the divergence of ratings poses a challenge for empirical research, as using one rater versus another may alter a study’s results and conclusions. Taken together, the ambiguity around ESG ratings represents a challenge for decision-makers trying to contribute to an environmentally sustainable and socially just economy.

Aggregate Confusion: The Divergence of ESG Ratings by Florian Berg, Julian F Kölbel, Roberto Rigobon :: SSRN

This isn’t just isolated research. Here’s an excerpt from a report by the European Union:

Sustainability-related rating providers measure, weight and score company sustainability risk and performance in different ways. This results in comparability issues of ratings across providers for the same target company even with similar starting data points. There are also three key types of bias typically encountered by sustainability-related ratings providers. The first, and most commonly referenced, is company size bias, where larger companies may obtain higher sustainability-related ratings because of the ability to dedicate more resources to non-financial disclosures. Second is geographical bias, where there is a geographical bias toward companies in regions with high reporting requirements. Third is industry bias, where sustainability-related ratings providers oversimplify industry weighting and company alignment. This bias and the variation that occurs across methodologies contribute to weak correlation or divergence across scores from different companies.

Study on sustainability-related ratings, data and research – European Union

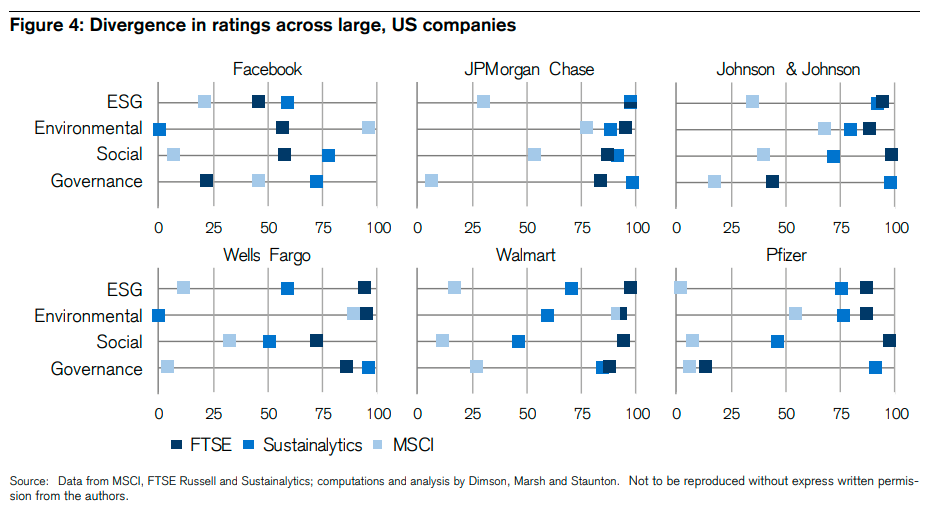

More recently, Elroy Dimson, Paul Marsh and Mike Staunton looked at ESG investing and found the same. They published their analysis in the Credit Suisse Global Investment Returns Yearbook.

Today, these ESG providers aren’t regulated by anyone. They don’t conform to any standards on measuring ESG issues, nor do they have an obligation to disclose their methodologies transparently. It’s shocking how quickly these data providers have grown and how influential they have become—their impact on the flow of capital markets is undeniable. And given just how profoundly flawed the data is, it’s scary even to imagine the implications of the data and ratings they provide. I’m hoping that this in itself will become a topic of study for researchers.

ESG data goldrush

Show me the incentive and I will show you the outcome.

If you want to know why something is happening, always look at the incentives. ESG is a massively profitable business. According to Opimas, a research firm, the ESG data market could hit the $1 billion mark this year. According to the EU report on sustainability which quotes Opimas, ESG data spending could’ve been as much as $745 million in 2021. That’s an astounding number for a trend that is just picking up some traction outside the institutional sphere. But these numbers are just estimates, but my gut says the number could be far higher.

Opimas research estimates that total spending on ‘ESG data’ globally was USD 617 million in 2019, and it is expected to reach USD 745 million by the end of 2020.14 It is forecasted that growth in spending will result in revenue generated through ‘data provisioning and benchmark licensing’ (‘ESG indices’) to be around USD 240 million in 2020 and in excess of USD 300 million in 2021, and that combined with ‘pure ESG data’ (‘ESG content’) will be around USD 525 million in 2020, possibly exceeding USD 630 million in 2021.

Study on sustainability-related ratings, data and research – European Union

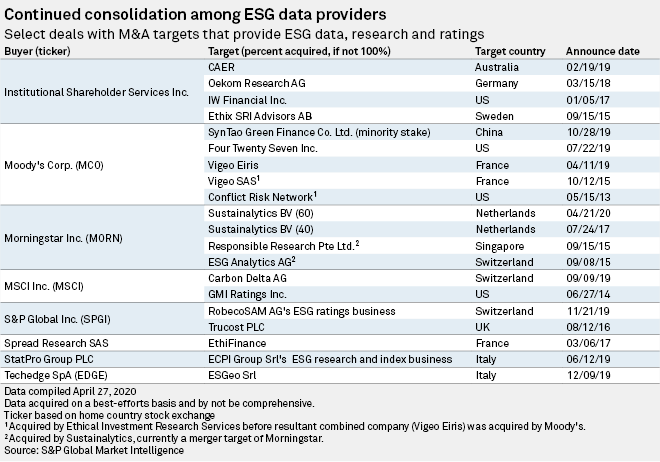

Given the money at stake, there has been a spate of mergers and acquisitions in the ESG data space. Morningstar with the Sutainalytics acquisition, S&P, and MSCI have been buying their way to dominance.

Flawed incentives

The other bigger issue here is that the bigger ESG data providers like MSCI, Morningstar, S&P, Refinitiv, and Bloomberg are also the biggest index providers globally. Trillions of dollars in equities and fixed income are benchmarked to the indices they have constructed. And these ESG indices are constructed on the same ESG data they sell which is flawed at best and absolutely useless at worst.

ESG data regulations

It’s the wild west today for ESG data providers. They aren’t regulated by anyone and aren’t answerable to anyone. But given that the European Union (EU) has been ahead in all things sustainability, the French and Dutch are pushing to regulate ESG data providers.

But other market regulators are yet to catch up. In the US, there are divergent approaches from the Securities and Exchange Commission (SEC), which is the market regulator and the Department of Labor (DOL), which regulates the corporate pension system, including 401K plans. The SEC hasn’t been overly concerned about the rise of ESG. But it has made some comments over the quality of ESG ratings and the labelling of ESG funds on whether they are true to their supposed green labels.

But informally, Hester Pierce, one of the commissioners on the SEC, has been vocally critical of what passes for ESG. She delivered a speech at the American Enterprise Institute, and this is perhaps, one of my favourite take for the clarity with which she eviscerates ESG sales pitches. Here’s the video and the text of the speech. I became a fan of Hester Pierce after reading this.

The passage that struck me the most:

We are seeing a similar scarlet letter phenomenon in today’s modern, but no less flawed world. In these remarks, I will focus specifically on the way in which corporations are being assessed according to Environmental, Social, and Governance (ESG) factors. Here too we see labeling based on incomplete information, public shaming, and shunning wrapped in moral rhetoric preached with cold-hearted, self-righteous oblivion to the consequences, which ultimately fall on real people. In our purportedly enlightened era, we pin scarlet letters on allegedly offending corporations without bothering much about facts and circumstances and seemingly without caring about the unwarranted harm such labeling can engender. After all, naming and shaming corporate villains is fun, trendy, and profitable.

SEC.gov | Scarlet Letters: Remarks before the American Enterprise Institute

The DOL, on the other hand, thinks that fiduciaries shouldn’t concern themselves with ESG factors when evaluating investment options in pension plans. There’s more to this, and I’ll expand on a landmark DOL regulation recently that has a lot of insight on ESG overall a little later.

Peeking under the hood of ESG funds

By now, I hope you have a working understanding of what this whole ESG thing is. The best way to understand things is to ignore the stories and look at the facts. Look, we are biologically hardwired to favour stories over facts. The reason is that the human brain is one of the hungriest organs in your body. Given that, it constantly looks to save power by looking for shortcuts. Looking for facts, processing them and arriving at a conclusion is a cognitively demanding task. So our brain has evolved to make shit up so that we have enough understanding of things.

And ESG is the best story ever told. It’s seductively brilliant. If you buy an ESG fund, you can save the planet, force companies to do good, and get market-beating returns. Hell, I’d fall for this if I wasn’t so cynical in life.

But if you set aside the story and look at the facts, here’s what you’ll find.

From the NSE whitepaper on the NSE ESG index:

Environmental, Social and Governance based investment strategy has gained popularity among investors globally. The underlying drive behind ESG theme based investing lies in generating superior risk adjusted returns from socially responsible, environment friendly and ethical firms. The construct of NIFTY100 ESG indices results in portfolio with similar sector exposure vis-à-vis NIFTY 100 (parent index), but with stock level ESG tilt. This results in portfolio with higher weightage towards companies with better ESG performance.

Now, if you look at the sales pitches of ESG funds, you’ll see tall tales like these funds are good for the society, the planet and other silly nonsense. But look at the indices, they are just sector and stock tilts over NSE 100, that’s it.

So, Indian fund managers, just by varying the stock weights between 2-6% from NSE 100, are solving corporate governance issues and are saving the planet? What absolute horseshit is this?

Here’s the best part. You get the privilege of paying 1-2% for getting what you can get for 0.15%.

Here’s the other problem

Every AMC offering an ESG fund says that you can save the world and generate higher returns. This begs the other question, are the other funds they are offering useless then? So, if ESG is so profitable, then shouldn’t every traditional fund be ESG?

Why are there separate ESG funds? If ESG is so good, these asset managers should integrate ESG in all the traditional funds, and everything should be ESG. Why have ESG funds which are good and traditional funds which are bad?

ESG is just active management in a new lungi!

Bullshit-there’s more of that than anything else in the world.

Marty Rubin

Let’s keep aside for a minute a hundred flaws with mainstream ESG funds. At the end of the day, ESG is just another form of active management, and active management is nightmarishly hard.

Maybe you’d have come across articles like this that showed ESG funds outperformed conventional funds. Blackrock published a report which said that 94% of sustainable indices outperformed their parent benchmarks. Morningstar went a step ahead and even called ESG funds as an “equity vaccine“.

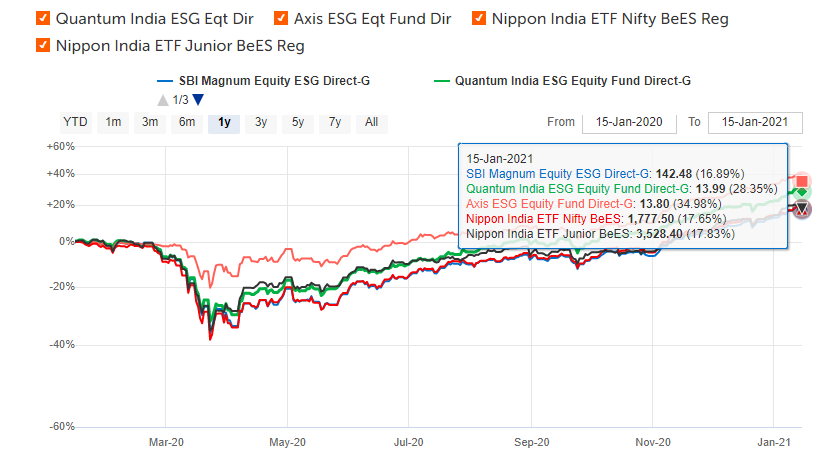

Turns out, 2 of the 3 oldest Indian ESG funds have outperformed Nifty 50 and the Next 50 by a handsome margin.

If you are thinking, ESG is awesome, hold just a minute. Similar to traditional funds, there ESG index funds and actively managed funds. The Mirae ESG ETF is an ESG index fund while the rest of the other ESG funds are actively managed. And that means they come with active management problems. And in the case of ESG funds, the active management problems are even amplified.

Pretty much all the research both globally and in India shows that there is very little persistence in mutual fund performance. The best performing fund in one year is most often than not, the worst-performing in another. I have written at length how over 50-80% of all active managers underperform their benchmarks. So, assuming hypothetically that ESG funds deliver superior performance (there’s no evidence), your odds of picking a good fund is very, very, very low!

Not to mention the fact that active management means underperformance. These funds can go a loooong time underperforming the benchmarks.

The other issue with active ESG funds, and this is an extension to what I wrote about dangerous flaws with ESG data. Pretty much all of the ESG funds rely on ESG data and ratings, and that data is pretty much useless. If you are an investor analysing these funds, there’s absolutely no way you can make an investment decision if the very thesis of a fund is flawed.

Similarly, with ESG index funds, the indices they track are based on the same useless ESG data. For example, the Mirae ESG ETF tracks the Nifty100 ESG Sector Leaders Index, and the index is constructed based on Sustainalytics ESG data. So garbage in, garbage out.

And the next issue is one that investors hardly bother about. AMCs are rife with various conflicts, from compensation structures to sweetheart relationships with distributors, and so on. At the end of the day, fresh money is the lifeblood of asset management. And to get new money, you either deliver benchmark beating performance or sell your fund by hook or crook.

Product pushers will couch ESG funds in moral rhetoric that you can do good, save the planet etc. But remember, when you are investing, you are putting your money to work in the hopes of achieving important goals like your kid’s education or retirement and so on. Please don’t fall for the sales pitches and invest in these funds with the misguided notion that you are making a difference with your money because, let me assure you, you are not.

Are you making a difference?

We’re now neck-deep in this ESG muck, and if you’ve followed me along this far, it’s going to get worse 😁

One of the biggest sales pitches of ESG funds is that they make a difference. And it’s easy to think that by investing in companies that are “good” and “green”, whatever that means, you are making a difference. But are you?

When you go buy a stock in the secondary market, it’s just an exchange between two different shareholders. The company isn’t even involved. So how are you making a difference? Well, the ESG advocates will tell you by not investing in poorly ranked ESG companies, they can raise the cost of capital.

The logic is that if ESG investors don’t invest in companies, that makes them look risky, and this raises the cost of capital for them because lenders may demand a higher interest rate and equity issuance becomes undesirable for the company.

But this is a bit of a stretch. Not all companies need capital all the time. In fact, companies excluded by ESG funds like tobacco, weapons manufactures, oil companies etc., tend to be cash-rich companies. Most of them don’t have to raise additional capital at all.

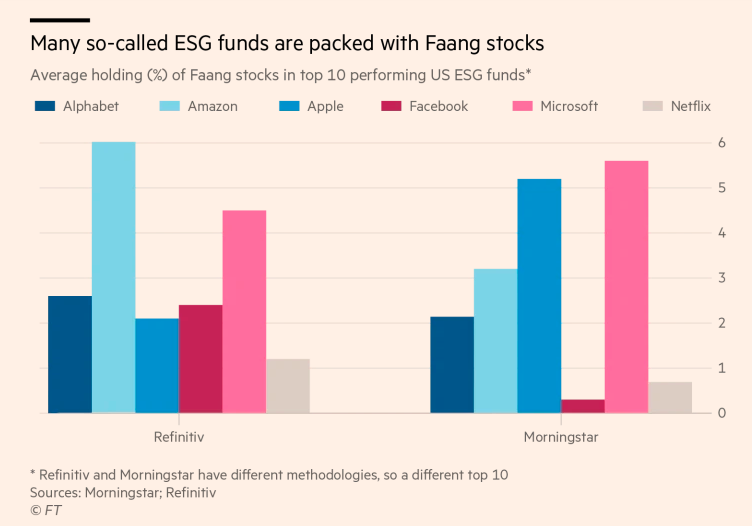

Today, most of the ESG funds both in India and the US are predominantly large-cap funds. While Indian ESG funds are financials heavy, US ESG funds tend to tech or FAANGM heavy. So, you need to wrestle with the tricky question of whether these companies got bigger because they care about ESG issues or they have a good ESG score because they are big and doing well? What causes what?

To sum it up, you are making exactly ZERO difference by investing in an ESG fund. The company could care less about you owning their stock or not because someone will. Perversely, by not owning certain stocks, you ensure that the next person who owns that stock is probably getting a higher return.

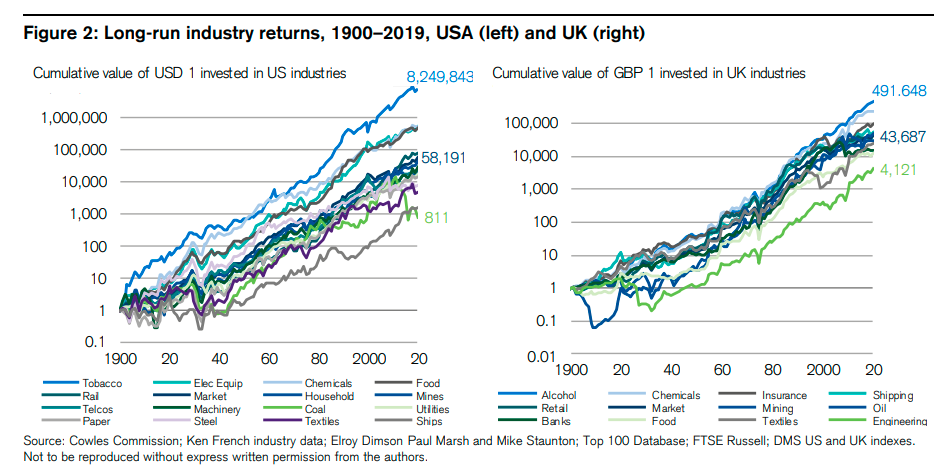

Here’s how some of the worst ESG companies have done in the long run:

What explains that performance? A study by David Blitz Robeco and Frank J. Fabozzi found that most of the performance was explained by the Fama and French factors like quality, profitability etc.

Blitz and Fabozzi (2017) confirm earlier findings that sin stocks have generated a significantly positive market-adjusted alpha. However, the alpha disappears, is insignificant, or even turns negative when they control not only for classic factors such as size, value and momentum, but also for the newer profitability and investment factors referred to by Fama and French (2015) as “quality”.

So, if you are not doing good and if you aren’t making it harder for companies to raise capital, what are you getting in return? Here’s Cliff Asness:

Put simply, if the virtuous are not raising the cost of capital to sinful projects, what are they doing? How are they actually affecting the world as they wish to? If the cost of capital isn’t also an expected return, what is it? This might be a painful reality to swallow for the virtuous. To get precisely what they want, which is less of the bad stuff occurring, they have to pay the sinful investors in the form of a higher expected return.16 Importantly, this isn’t an accidental byproduct of ESG investing. It’s the only way all this really matters one drop to the central issue – how much bad stuff happens. If the discount rate used by sinful companies isn’t higher as a result of constraints on holding sinful stocks then there was no impact. And, if the discount rate on sin is now higher, the sinful investors make more going forward than otherwise.

Virtue Is its Own Reward: Or, One Man’s Ceiling Is Another Man’s Floor (aqr.com) – Cliff Asness

Frankly, it sucks that the virtuous have to accept a lower expected return to do good, and perhaps sucks even more that they have to accept the sinful getting a higher one.17 ,18 Well, embrace the suck as without it there is no effect on the world, no good deed done at all. Perhaps this necessary sacrifice is why it’s called “virtue.”

So, all you are getting out of investing in ESG is the benefit of feeling good. You can make more of a difference by calling out the unethical practices of companies on social media or writing about them than buying a useless ESG fund.

Now, you might say that your fund can use its voting rights to influence management. Sir, nice thought. But I’ll tell you the reality. Read on.

The mother of all ironies

In all this nonsense, one thing that gets on my nerves is that asset managers are preaching the virtues of ESG. Asset managers are among the most unethical actors in the finance ecosystem. Asset managers preaching ESG is a bit like smoking companies preaching the importance of health and wellness.

I can’t believe what you say, because I see what you do.

James Baldwin

In India alone, AMCs have been responsible for:

- Creating and selling sub-par mutual funds

- Overcharging

- Index hugging while price gouging

- Poor risk management practices. Most notably in debt funds that have led to lakhs of people losing money

- Allowing distributors to mis-sell products while doing nothing Most notably, several leading AMCs did nothing when dividend plans of balanced funds were mis-sold as guaranteed income products to retirees

- Bank owned AMCs are notorious for mis-selling their funds through their banking channels

- Sweetheart deals with major distributors and making payments that may not be in line with regulations and downright unethical

- Using funds meant for investor awareness to compensate intermediaries

- Foreign trips to distributors and advisors paid from the investors’ pockets

And let’s not forget that there is just one female-led AMC in India. And see if you can remember a “star female fund manager”. This industry has been the absolute worst when it comes to gender diversity. It’s an old and wrinkled men’s club.

If we just judged AMCs by how much money they spend on useless made in China gifts on Diwali and New Year and the plastic waste they generate, their hypocrisy would be evident.

Here’s another irony, which is almost funny. The reason why Axis, ICICI, and Kotak have been able to raise Rs 1000 to Rs 1500 crores in their ESG funds is that they have blatantly churned and mis-sold those funds through their banking channels and distributors. You can ask anyone in the mutual fund industry, and they won’t be able to deny this.

At a time when mutual funds have seen seven months of continuous outflows, how else can 3 ESG funds from ICICI, Kotak, and Birla raise over Rs 4000 crores? That, my dear investors, is how ESG friendly your friendly neighbourhood AMC is.

If AMCs are judged and assigned ESG scores, they would, in my book, have worse ESG scores than tobacco and oil companies, with very few exceptions. Not just that, these guys at these AMCs won’t know what ESG is if it came and slapped them in the face.

This might seem like an overly cynical critique of the asset management industry. Sure, I have just about six good things to say about Indian AMCs but that doesn’t make it any less true. All it takes to verify whatever I have written is just one google search or a conversation with someone from the industry.

Globally it’s the same. Asset managers in the US and UK have been involved in some of the most egregiously unethical practices. Acts that have damaged the financial outcomes of millions of average investors.

Proxy voting

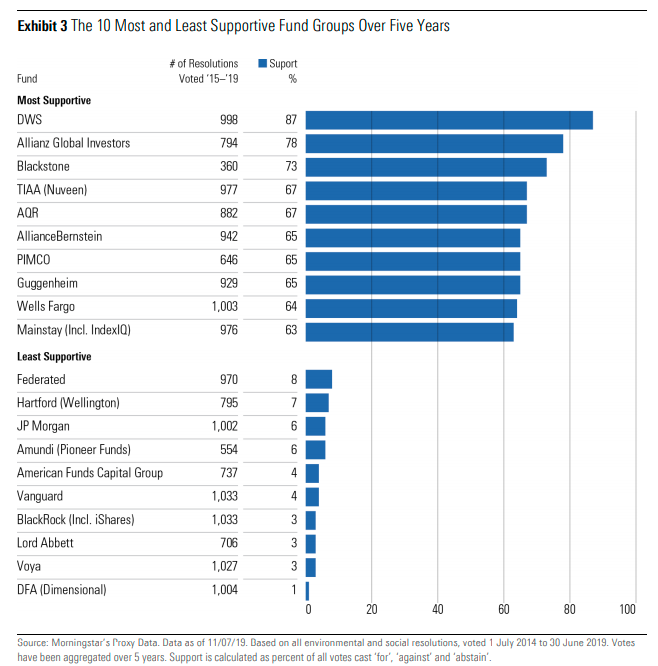

Now, coming back to the question of whether asset managers are using their voting rights to influence company managements, here’s what Morningstar found:

Blackrock and Vanguard, the 2 biggest asset managers on the planet, have the worst records. If you add JP Morgan, American Funds, and DFA, these AMCs collectively manager nearly $15 trillion in assets.

While Larry Fink, the CEO of Blackrock has become something of a poster child for ESG and has been writing letter after letter to CEOs asking them to do good, his own actions don’t quite match up. Here’s what he wrote in a recent letter:

In a letter to our clients today, BlackRock announced a number of initiatives to place sustainability at the center of our investment approach, including: making sustainability integral to portfolio construction and risk management; exiting investments that present a high sustainability-related risk, such as thermal coal producers; launching new investment products that screen fossil fuels; and strengthening our commitment to sustainability and transparency in our investment stewardship activities.

We don’t have such a readymade study in India, but I glanced at the voting records of AMCs with ESG funds. By my guesstimate, 99% of the time, they vote with the management. Moreover, AMCs outsource the voting to external proxy voting advisers and vote based on their recommendations. If you think that your AMC has a dedicated team of employees analysing company proposals, doing due diligence and then voting to save the planet, you’re bloody wrong!

The irony is that they may say Milton Friedman was wrong, but AMCs are in the same business of making profits for their shareholders. AMCs at the end of the day are profit-seeking entities. Profits for their owners and shareholders will always be a priority over whether they are doing right by the investors and doing good for the world. Of course, there will be a few exceptions and most of often than not, these exceptions tend to be smaller AMCs or specialized boutiques.

Moreover, who died and made AMCs the arbiters of ESG issues? What even makes them qualified to judge these issues? These are the same bloody managers who are having a hard time beating their benchmarks and doing the job they are so handsomely paid for.

It’s like they aren’t even pretending not be hypocrites anymore:

Moreover, for all the talk about ESG, not a single asset manager on the planet shows tangible metrics on how they are actually making a difference. If the asset managers were indeed so concerned about doing the right, they would go the extra mile to quantify their impact through their funds.

50 shades of ESG

There is no globally accepted definition of what ESG. It pretty much lies in the eyes of the beholder. That means ESG can be implemented in 100 different ways. What I have so far railed against is that mainstream ESG is bullshit. But managers are integrating ESG data in their existing analyses in a myriad of ways.

The problem with the ESG product of large asset managers is that they promise something to everyone and specifically nothing to no one. Mass-produced “ESG” products will always be useless and are largely meant to be shelf filler products so that the asset managers don’t miss out on taking money from conscious customers. They are also a really easy way for asset managers to virtue signal their green credentials.

Today, smaller boutique asset managers are implementing ESG in some really interesting ways. For example, here’s how Ash Park, a specialist asset manager that focussed on consumer staples, implements ESG:

We regard ESG issues as being fully-integrated into our approach to portfolio management. We aim to own each of the stocks in our portfolio over the long term and, if companies cannot deal sensibly and responsibly with important environmental and social challenges, then the steady long-term growth that we expect is put at significant risk. When we see potential problems, or areas in which we think our portfolio companies could and should improve, we will engage with managements; we believe our expertise and the long relationships we have had with many of our holdings mean we punch significantly above our weight when it comes to getting our voice hear

They don’t believe in selling companies just because they are bad but rather engage with them. That’s a better way to bring about change than sell companies because selling doesn’t do anything.

Here’s how Honeytree, a Canadian asset manager, approaches sustainable ESG investing. Liz is also a great follow on Twitter for all things ESG:

To me, the some of the best implementations of ESG would be :

Activist ESG PMS’ and AIFs (hedge funds): These need to be funds with a self-selected set of investors that focus on narrow and specific issues. These funds can build concentrated positions in “bad” or “sinning” companies and harass the managements into changing. This is nothing but activist investing. They’d need patient capital that can withstand long bouts of underperformance and hence the need for self-selected investors. Such structures would almost be operating like NGOs.

Debt funds: Green or sustainable debt funds that only invest in green bonds and other sustainability linked bonds. We already have these, but they’re loaded with greenwashed bonds. There is a space for someone to become specialized in this space and build a brand around it.

If AMCs don’t want to do bullshit ESG, they can do the same. Launch ESG funds that have a clearly specified purpose and specify issues they want to focus and clearly communicate them to the investors that there might be a performance penalty. This needs to be backed with data and research and requires building specialized internal teams that can engage with companies on a sustained basis.

Just launching another ESG fund based on junk ESG data or ratings is pointless. The advantage of launching a fund that could actually focus on issues and engage with management is that the AMCs can charge a higher fee.

Long short ESG focussed funds: Assuming that a company is bad, if you sell the stock, the company could care less. But if you short the company’s stock, that’s a better expression and moreover, companies hate short-sellers. This is a much better way to get companies to behave. Here’s a 130/30 example of how such a fund could work by AQR.

Short sellers

Perhaps, the best form of ESG to my mind are short-sellers that take on fraudulent companies. Not just the big name shorts like Enron by Jim Chanos, Michael Burry’s subprime shorts. But also those chindi chor companies like the Chinese reverse listings shown in the Netflix documentary The China Hustle that are lure among small mom and pop retail investors. Most recently, short selling firm Hindenburg exposed Nikola, the much hyped Tesla competitor to be a fraud.

In India, shorting is hard, but hopefully, we will see this change over time. Shorting to me is the ultimate expression of ESG because it tends to evoke visceral hatred among the management of companies and also leads to a lot of press. This tends to increase scrutiny of other peer companies in a sector too.

Just saying you’re an ESG fund is meaningless because ESG could mean a 100 different things. And these implementations can come with poor performance. At least I am not buying this story of doing good and earn higher returns as well.

Alternative data

Perhaps the best view of ESG that I have come across is to think of ESG as alternate data, thanks to this brilliant paper by Ashby H. B. Monk, Marcel Prins and Dane Rook.

In the recent decade or so, generating alpha in the public markets has become incredibly tough due to various reasons like increasing relative skill levels of market participants, the explosion of free data, cheap computing power, and generally increasing market efficiency.

Given this reality, fund managers, hedge funds etc. have been looking towards alternative data sources like satellite imagery, credit card spending data, social media chatter, trucking data, shipping data etc. to gain an edge.

Given that ESG data is non-financial data, thinking of it as alternative data without polluting it with things like “creating change”, “saving the world” etc., seems apt to me. But this comes with its own challenges like the quality of data, greenwashing and so on.

I think this will become a theme among quantitative asset managers. Given the lack of standardized ESG definitions, ESG data could potentially be a source of higher returns. But slowly, as standards are imposed and as the markets react and price things, these edges could vanish. For example, there have been numerous examples of asset managers using Glassdoor data as a proxy for employee satisfaction, gender diversity insights, management quality, etc. But a lot of people are of the view that that predictive power of this has been arbitraged away.

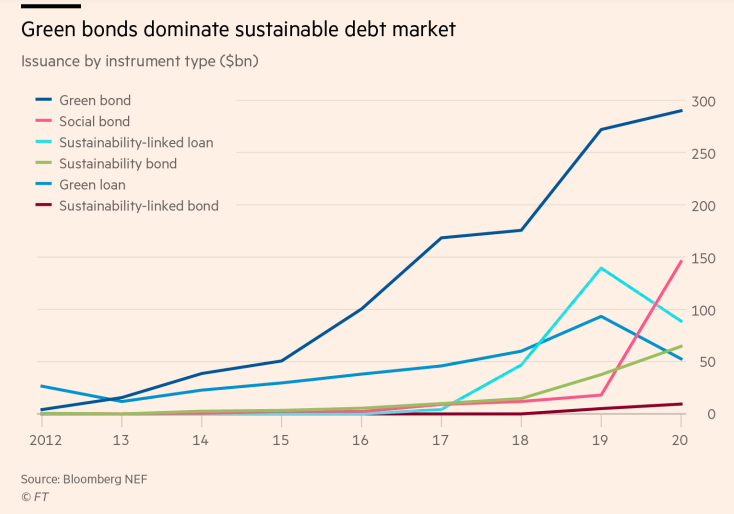

Arguably, compared to equities, ESG debt can actually make a difference. But, yes, there’s always a but. There have been widespread concerns about greenwashing in green and sustainability bonds.

Fixed income

So far, whatever I have spoken about ESG has been from an equity lens, but ESG isn’t limited to equities. ESG is also a growing trend in the fixed income space. Companies and various organisations now issue green bonds which are specifically meant to finance environmental projects.

Similarly, there are various other types of bonds like sustainability linked bonds that are linked to a tangible outcome. For example, a Brazilian pulp maker late last year issued a sustainability linked bond subject to greenhouse gas reductions. If the company couldn’t meet the stated outcome, the bond coupon would increase by a specified percentage.

But not all green bonds result in carbon reduction as this analysis by The Bank for International Settlements found:

The current system of green bond labels does not necessarily guarantee a material reduction in carbon emissions. Indeed, these labels would signal emission reductions only if the relevant projects were to transform the activities of the bond issuer radically enough for its carbon emissions to fall. But, as we show in the next section, green bond labels are not associated with falling or even comparatively low carbon emissions at the firm level.

If the problem with ESG data in equites is it’s utter uselessness, when it comes green bonds, the bigger issue is grenwashing. I found this quote in this FT article particularly telling:

Chris Bowie, a portfolio manager at TwentyFour Asset Management, said that if a bulk of an issuer’s business is in “dirty” industries, “and they are asking you to finance the clean bit, I’m not sure it’s really influencing them to change their behaviour.”

FT

Like with most things ESG, even ESG in fixed income is largely a joke

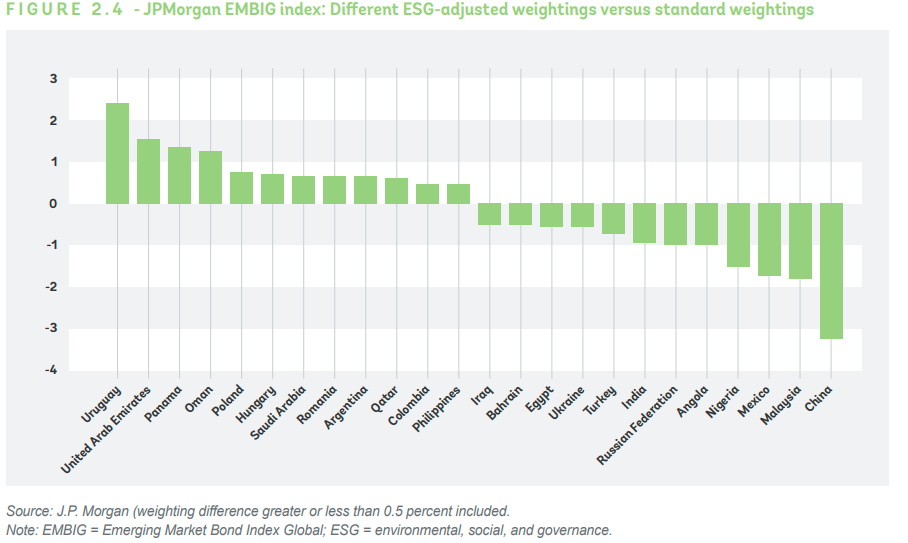

These are ESG adjusted country weights in the JPMorgan EMBIG (Emerging Market Bond Index Global) relative to the standard weights. Hungary and Saudi Arabia have higher weights than India, go figure.

Green finance also suffers from the same issues with data quality that makes it hard for investors and allocators to evaluate the green credentials of a bond or a company.

Another instance of greenwashing took place when the Chinese government issued Green Bonds to finance coal-efficiency projects that find ways to burn fossil fuels more effectively. Similarly, a Madrid-based oil and gas company named Repsol issued a set of “Green Bonds” that were used for making their oil refineries more efficient. Although technically still working towards energy efficiency, these projects are not helping the environment to the extent that issuers will often claim.

Are Green Bonds as Good as They Sound? – Berkley Economic Review

Not to keep harping on the negatives but will green finance become an effective avenue to channel money to initiatives that can bring about change and whose impact can be tangibly measured? I remain sceptical, but stringent regulations, oversight and better data can curb the downright unethical practices by issuers currently.

For retail investors

After ranting and raving let me start wrapping this up. If you are an investor, ESG is all about expressing your values. Asset managers peddling their funds with the sales pitch of doing good are lying and what they are saying is absolute nonsense. At the end of the day, ESG is just about owning something that conforms to your values and that’s it. And this, no matter who says anything, can have a performance penalty.

I think ESG, works best when it is implemented in a bespoke and customized way. On the retail side, we are now seeing ESG focused robo advisers like EarthFolio which offers full ESG portfolios. Traditional robos like Betterment, Wealthsimple have also started offering ESG or some version of sustainable portfolios.

On the advisor tech side, all major investment tech providers have begun offering ESG solutions. There are now dedicated ESG focussed platforms for advisers like Ethic.

Direct indexing

Any conversation about ESG would be incomplete without talking about direct and custom indexing. This might seem like a weird tangent but stick with me. With mutual funds, common people worldwide got easy access to equities, bonds, commodities and real estate at a relatively low cost. ETFs were the next evolution of mutual funds, and they were tradable in real-time. The question on the lot of people’s mind has been what comes after ETFs?

A lot of people have been touting “Direct Indexing” as the next big thing. In simple terms, direct indexing is basically owning all the stocks of an index directly instead of just buying an index fund or an ETF. Why would anyone want to do it, you might be wondering. There are few use cases such as tax-loss harvesting which isn’t possible inside an ETF or a mutual fund. The other use case is expressing your views. Let’s say, you like an index fund but have a problem with gun manufactures, you can own the index minus the gun manufacturers.

Which means direct indexing is perfect for ESG. You can take any broad market index and apply exclusionary screens to screen out stocks that don’t match your values. For example, it could be guns, oil, tech etc. Not just that, this also allows you to apply factor overlays like value, momentum, etc. on top of the ESG screens you apply.

You could also build your own custom ESG index suited to your value and belief system, have your own index rules and buy the individual securities accordingly. With fractional investing now become widely accessible in the US, mimicking an index outside an ETF or a mutual fund wrapper is easy.

Similarly, there’s another variant of direct indexing called custom indexing. The folks at OSAM have built a platform called Canvas that allows advisors to essentially build their own indexes with defined rules and invest based on that.

Like standard indexes, Custom Indexes also invest and rebalance according to a defined methodology. But with Custom Indexes, the methodology is personalized based on an investor’s circumstances and preferences and can be easily adjusted as an investor’s circumstances change. This flexibility is possible because Custom Indexes are implemented through separate accounts, where investors can directly own a custom mix of individual stocks and bonds rather than indirectly owning positions through a collection of funds and ETFs

This makes implementing ESG a whole easier because it would allow advisors to tailor portfolios according to investors values and beliefs. Today this is a bit hard with ESG funds and ETFs.

Oh, by the way, fractional investing isn’t allowed in India. The closest thing we have to direct indexing in India is smallcase, which allows you to build your own custom portfolios. But with ESG becoming a megatrend, direct indexing and custom indexing are bound to become popular because of that.

ESG in India

ESG is not even a thing in India, and these are very very early days. SEBI had mandated the top 100 companies in 2012 to publish something called a Business Responsibility Report (BRR). This was later extended to the top 1000 companies last year.

BRR required companies to disclose some basic financial and employee data and policies for various social and governance issues. It wasn’t comprehensive, but nonetheless, it was a start. In August 2020, it issued a consultation paper on a new BRR format which is far more comprehensive than the existing one.

As for ESG funds, we have 7 broad ESG funds. Indian AMCs have zero idea about ESG nor do they care. The first ESG fund in India, the SBI ESG fund was an old fund that was recategorized as an ESG fund. This was because SEBI had bought in the scheme recategorization rules that said that AMCs could only have one fund per category except for thematic funds, index funds, and FOFs. So SBI which I think had two large-cap funds turned one into an ESG fund. 😂

The next couple of products were launched because ESG as a trend was getting hot globally and what happens globally, we import it here. And more recently, ICICI, Birla, and Kotak launched ESG funds because they saw massive outflows. They launched these NFOs and like I wrote earlier massively mis-sold them through their parent banking arms to stop the outflows from their other funds.

We will slowly see more AMCs line up and launch ESG funds, just to fill the category. But make no mistake, except for seven investors, nobody cares about ESG in India!

ESG and fiduciary duty

This is perhaps the most important question in my view but the least discussed. The question of whether an investment adviser is being a fiduciary if he recommend ESG funds.

This point seems weird and irrelevant to you, but today ESG is hot among advisers in the US and maybe the EU to some extent. So much so that, there are now advisers who’ve built their entire practices around some version of ESG and sustainable investing. I don’t see this happening in India anytime soon, but it pays to know.

So, coming back to the question at hand, here’s how I look at it. An advisor is acting as fiduciary if he honestly explains to his or her clients the flaws of ESG, the issues with the data being used, the real impact the investor is having in the real world, and the possible performance penalties because ESG is active management at the end of the day.

If an advisor instead just uses the same marketing sales pitch that the investor is doing good for the world and also getting high returns, then he is violating his fiduciary duty. Of course, this doesn’t apply to distributors because they don’t have a fiduciary duty. They just have to abide by a suitability standard.

ESG has become a such a trend that the US Department of Labor (DOL) last year came up with a rule on how plan fiduciaries – people who oversee retirement plans should consider ESG issues when selecting investments. For context, DOL oversees the employee pension system in the US, including 401K plans which combined have over $10 trillion assets.

Now, this might seem like it’s irrelevant if you’re having your coffee and reading this India. But I think, eventually, we’ll have the same debate here as well so, bear with me.

In June last year The DOL proposed the following rule and sought comments:

The Department’s aim is to assist ERISA fiduciaries by establishing clear regulatory guideposts for plan fiduciaries in light of recent trends involving ESG investing that the Department is concerned may lead ERISA plan fiduciaries to choose investments or investment courses of action to promote environmental, social, and public policy goals unrelated to the interests of plan participants and beneficiaries in financial benefits from the plan and expose plan participants and beneficiaries to inappropriate investment risks.

They basically wanted plan sponsors (people who manage pension plans) to choose investment options based on risk and return characteristics and nothing else. Sponsors shouldn’t select ESG investments if it led to lower returns or higher risk compared to similar non ESG investments. The other insinuation was that this prohibited sponsors from focusing on other objectives like “doing good” or other ESG issues instead of the retirement security of the employees in the plans.

Eugene Scalia, the son of the late conservative US supreme justice Antonin Scalia, was heading DOL at the time. When the rule was proposed, he also penned an op-ed in WSJ and wrote:

The department’s proposed rule reminds plan providers that it is unlawful to sacrifice returns, or accept additional risk, through investments intended to promote a social or political end. Sometimes, ESG factors will bear on an investment’s value. To give an obvious example, if a factory is leaching toxic chemicals into groundwater, lawsuits and regulatory action are likely to follow, sapping profits. A corporation with dysfunctional management will also typically be a poor investment.

WSJ

The entire asset management industry was up in arms. Apparently, more than 95% of the nearly 8700 comments received on the proposal were against it. Predictably, given that this came under the Trump administration, this became a political issue. Allegations were made that this was to promote the interests of the Oil industry.

The DOL went ahead and notified the final rule.

Fiduciaries must evaluate investments and investment courses of action based solely on pecuniary factors—financial considerations that have a material effect on the risk and/or return of an investment based on appropriate investment horizons consistent with the plan’s investment objectives and funding policy.

DOL ESG Rule

In the final amendment, instead of explicitly mentioning ESG, the DOL used the terms “pecuniary” and “non-pecuniary” factors. Now plan fiduciaries are only supposed to choose investments based on factors that have an impact on risk and return. If they choose an investment based on non-pecuniary factors, they can be sued. Lawsuits against plan sponsors have dramatically increased in the US. People are suing them for high fees, useless active funds that haven’t beaten index funds and so on.

What most people don’t know is that this is one of the reasons for the rise of index funds. If only we could sue Indian AMCs for not being able to justify the high fees they charge that borders on racketeering.

Sorry for the US example and legal mumbo jumbo. The reason why I wrote about this is to explain that ESG considerations can have real-world consequences on important goals like retirement.

The truth is, ESG is such a broad and haphazard concept that without strong fiduciary standards, it risks becoming a convenient excuse for those same fund managers to underperform their benchmarks while also charging higher fees.

Jordan N. Boslego, CFA, ESG researcher

Ok, so ESG is useless then?

Yes, and no.

NO

I don’t mean to mess with you, let me explain. If you had asked me this question 6 months ago, I would’ve told you it was 100% useless. But since then, I’ve come down to 95%.

Look, 99.99% of so-called “ESG” funds are utterly flawed, and worse yet, they are mis-sold, because the asset managers clearly know the flaws with the data being used. That’s downright dishonest and unethical. Moreover, the sales pitches that they are good for you and the universe is misleading. As I wrote earlier, you buying stocks in the secondary markets has very little to no impact.

The only real possibility of you making a change is through sustainable and green debt funds but we don’t have those in India. And even if we did, just like equities, these green and sustainable bonds suffer from similar issues as I have written above.

Yes

A lot of advisors and ESG proponents say that ESG is about investing according to the investor’s values and beliefs and that it helps them behave. I personally don’t fully agree with it, but people are unique. So, if you are an investor and you don’t want your money to be associated with a bad company in any way, sure, you can remove it if it helps your conscience.

On the other hand, if you are an investor and investing in a way that reflects your values and helps you stick with an ESG fund for the long term, then, by all means, invest in it.

But

Yes, there’s always a butt. You must be absolutely sure about the trade-offs here. ESG is active management, and 80% of all active managers suck. When you make an active choice, you run the risk of underperforming a simple index fund for long stretches of time. The other thing is that these funds are based on flawed methodologies and utterly useless data.

As long as you are aware of these shortcomings, feel free to invest.

Goddamnit! Is there no way I can make a difference with my investments?

Buying an ESG fund and hoping to make a difference is like imagining losing weight without going to the gym, it ain’t gonna happen.

The best way you can actually make a difference is not to waste time bothering with the utterly useless mainstream ESG funds. Instead, invest in low-cost index funds and then donate the difference in expense ratio to a charity that supports causes that matter to you.

Better yet, with the money you save by not investing in ESG funds, you can spend that on planting some saplings if you have space and nurture them. Those trees alone will make more difference than you investing in an ESG fund for a lifetime. In a surprising move, ICICI Pru announced they are planting 50,000 trees, one each for the 50,000 investors in its fund. See, that at least means, the investors in ICICI Pru ESG fund, even though it is absolutely flawed are making a difference. The fund won’t but the trees will.

Let me be absolutely clear. The only difference you are making in investing in most ESG funds is making the AMCs richer.

I wish we had someone like Impactshares in India. It is a unique non-profit AMC that offers ETFs tied to issues like racial justice, women empowerment, and UN Sustainable Development Goals (SDGs). But the unique thing is that it donates all the profits to the respective charitable organizations fighting for these issues. It’s a brilliant model that actually makes a tangible model.

But it is incredibly hard for such asset managers to raise enough money to survive. I’m rooting for them to make it big.

Everything will be ESG