The good thing about the internet is that it gave everyone a voice. The bad thing is that everyone now has a voice. What do you get when everyone has a voice? An age of abundance, an abundance of, for the lack of a stronger word, horseshit! This is also an age of bullshit, the internet has been weaponized to spread disinformation, sow discord, and amplify stupidity. And no, this isn’t a uniquely contemporary phenomenon. We, humans, have been bullshitting since the day we were created, it’s just that bullshit didn’t spread much or took a long time to. But the internet has democratized the ability to bullshit with a few tweets, Facebook posts, tik-toks and taka-taks.

This is an age of abundance of all things, from cheap Chinese plastic shit, cutting-edge sports shoes made by Vietnamese kids whose first word after they are born is Nike, diet and health fads, productivity porn, stress and anxiety.

Yep, people are stressed, anxious and freaked out. Stress and anxiety as benign as they seem are killers. I don’t know if I’d be right in saying that this is the most stressed out generation ever, I don’t know. Maybe in the 1800s and 1900s, people didn’t live long enough to be stressed and be riddled with anxiety because they most likely would’ve been dead by their 30s from snakebites when went out to pee in a bush or from diarrhoea (yes, diarrhoea kills!).

In the recent decade or so, there’s been an increasing awareness about mental health but it’s still a taboo in large parts of the world to talk about mental issues but times are a-changing, slowly. You might have come across articles that cite studies like this one, for example, which found the following:

One in seven Indians were affected by mental disorders of varying severity in 2017. The proportional contribution of mental disorders to the total disease burden in India has almost doubled since 1990.

In 2017, 197·3 million (95% UI 178·4–216·4) people had mental disorders in India, including 45·7 million (42·4–49·8) with depressive disorders and 44·9 million (41·2–48·9) with anxiety disorders.

Or this study by WHO:

In India, the National Mental Health Survey 2015-16 reveals that nearly 15% Indian adults need active intervention for one or more mental health issues and one in 20 Indians suffers from depression. It is estimated that in 2012, India had over 258,000 suicides, with the age-group of 15-49 years being most affected.

While serious issues like depression etc are increasingly becoming a part of mainstream conversations and rightfully so, anxiety issues and stress caused by money don’t really get much attention in my view. Financial stress and anxiety can be equally dangerous and can kill!

As you are reading this, it might seem like I am bullshitting that money worries are dangerous, and if you had told me the same thing last month, I’d have cracked an inappropriate joke. But don’t take my word for it, this paper found that market volatility can literally make you sick:

Over roughly three decades, we provide evidence that daily fluctuations in stock

prices has an almost immediate impact on the physical health of investors, with sharp

price declines increasing hospitalization rates over the next two days. The effect is

particularly strong for conditions related to mental health such as anxiety, suggesting

that concern over shocks to future, in addition to current, consumption influences an

investor’s instantaneous perception of well being.

But what causes financial anxiety? It’s something of a cycle, poor mental health can cause financial anxiety and financial anxiety can lead to poor mental health. Financial stress and anxiety could be a result of 100 different things, but to me of late, it seems like, external triggers are causing more and more financial anxiety. Not just that, the pandemic we are going through has made it extremely worse.

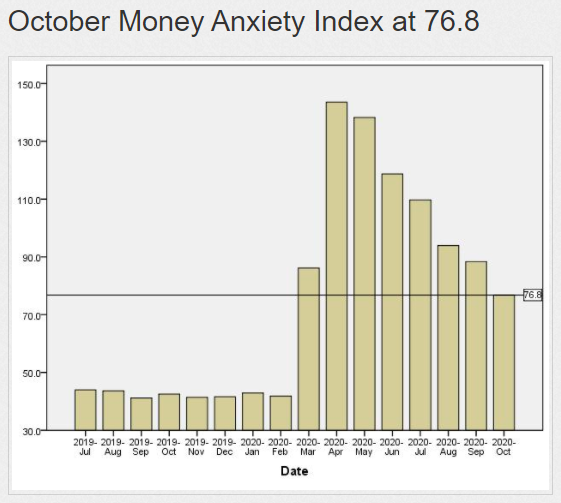

Dan Geller, a behavioral economist maintains a Money Anxiety Index in the US, and look at the readings. We are starved for data in the Indian context, but I’d bet it would be the same, if not worse even if you take the data with a pinch of salt.

Our complicated relationship with money

One of the root causes of anxiety is also our dysfunctional relationship with money. This is best summed up by the asinine saying “never ask a woman her age, a man his salary” we all would have no doubt heard in our lives at some point. Our views are a result of our culture, experiences, the environment we grew up in, education, what comics we read when we were young – Superman or Playboy and a hundred other things.

Let me give you a simple example, even to this day, in most middle-class south Indian families, Investing in the stock market is considered gambling, not trading or investing. Parents tell their kids to put that money in chit funds or to buy land, gold etc. And most often than not, the views about money that we learn as a result of the environment we group up in, tend to stick. People tend not to change their views and this ends up causing all sort of issues down the line. The thing about bad views about money is that the damage is slow but pernicious. People don’t really worry until it’s too late. It’s like someone who invests in FDs for 20-30 years because he thought the stock market was gambling and if he realizes that he was wrong in his 50s, he’s already too late.

The other issue is that talking about money is looked at the same way as talking about some really depraved kinky sex, it’s a mega taboo. Not just with others, people don’t even talk about money with their parents and partners even. When people, bloggers etc write about something about personal finance, they often write as if they’ve figured out everything about money and they are two zeroes away from being Warren Buffet, let me assure you, that’s not the case here.

I’m writing about the fact that talking about money is hard not because I’ve figured out how to, hell no. I am writing it precisely because I know how hard it is and I have never had a straight conversation about some as basic as how much my salary is with my parents. Not just that, as someone who has in the financial services industry and has some sense of money mistakes, I have zero clues about the finances of my parents and this is something I intend to correct soon. But I am pretty sure this will be opening a Pandora’s box. And I am also pretty sure, had I opened this box earlier, the fallout would’ve been far lesser and there would’ve been far more time to fix some of the issues.

What I’ve found is that, for all our cultural differences, one thing we seem to have in common is that we were taught to never talk about it! We were told it was impolite. Unseemly. A faux pas. Fascinatingly, it’s totally all right to talk about stock markets or the economy in general. The financial networks talk way too much about that version of money. But that’s different. When it comes to talking about your money… the message is …. just don’t.

Carl Richards/NYT

This can be due to a lot of reasons, because of our insecurities, because of fears of comparisons – both your own and those by the people you are talking to. People don’t talk about money because deep down they’re afraid of being compared to someone who makes more than them. Because let’s face it, being comfortable with your money situation isn’t an easy thing unless you’re Buddha. It’s never enough because of the never-ending rat race we’ve signed up for. And we most likely will die being unhappy with money than being satisfied. I don’t think that’s necessarily wrong, but I don’t think that’s right either. It’s important to get to a place where we can at least be a little satisfied with our money situations if not attain nirvana.

Our views about money are as much of others as they are our own. Think about all the times you bought some stock or invested a certain way because you’ve benchmarked yourself to someone else. As much as we hate to admit it, we exhibit strong herd behaviour when it comes to money. We’re all fricking Warren Buffett’s in our minds when in reality we most often than not are idiots.

And when it comes to money, we love signalling even if a particular decision might not make sense at all. This can be seen when people invest in products like PMS’ and AIFs where there’s a certain premium attached to the products. The inference here is that, if you are investing in a PMS or an AIF, you are rich and sophisticated. And it makes for a nice thing to show-off at the next family dinner even if that particular PMS or AIF manager is underperforming a fixed deposit. In the US, Billions of dollars belonging to pensions are stuck in useless hedge funds today, not because their horrendous performance might mean revert. But because of herd behaviour and the fact that the pension board won’t fire you for putting money to work with a superstar hedge fund manager. Even the smartest institutions are as dumb as the dumbest lay investor.

This tendency of ours to view our bank balances, our investments, the things we buy, the way we spend in comparison to others is probably one of the greatest sources of anxiety. As I said, I don’t know if anybody can live their life comparison free, we are social animals after all this behaviour is par for the course in a social construct, but doesn’t make it right.

There’s nothing in this world, which will so violently distort a man’s judgment more than the sight of his neighbour getting rich.

J.P. Morgan, 1907

Every goddamn rupee we spend most often than not has an element of “because he/they did it” in it. If that’s not the case, congratulations you are 67% away from being a modern-day Buddha, and attaining enlightenment. You can start picking out a banyan tree sapling for your courtyard and a silk loincloth.

And the end result of this dysfunctional relationship with money? Read on.

Personal finance: The rise of the bullshitters

50 years ago, you only had to deal with money advice from your parents, friends and probably that pesky neighbour LIC uncle who wanted to scam you into some policy. But today, things are different. One of the biggest problems for investors today is the sheer amount of information and noise.

To put that in context, there are over 100 crore search results for the term “personal finance tips”. You’ll need 100 crore lifetimes and then some to scroll through all of those tips. And then, of course, you have to put up with all the advice from your parents, friends, colleagues, books, TV ads, podcasts, Twitter gurus, salesmen, distributors, advisers, bank RMs and this can overwhelm, intimidate and confuse even the smartest.

And when the volume increases, inevitably, the quality of the content decreases. The internet has not only democratized access to information, but also the pathway to gurudom. In the past 5 years, millions of new personal finance gurus have been minted who are on a self-proclaimed mission to save investors from darkness and ruin.

But what gives rise to these gurus? At some level, they tap into your inner fears, anxiety and lack of awareness. Let’s take the example of all the godmen and babas, why do people follow these people, even idiots like this

These people tap into our insecurities, fears, and the unknown and promise things that which we seek and provide a false sense of comfort, It’s the same with personal finance. In the last 2-3 decades, financial markets around the globe have evolved dramatically. The rise of electronic trading, retirement accounts, discount brokerages, mutual funds and ETFs have democratized access to the stock markets to the masses. And the investors base, although still small has expanded dramatically and continues to increase at a good pace (except India) as new-age financial services firms AKA the likes of your Robinhood, Betterment, Zerodha, smallcase, Nutmeg, Scalable Capital etc take a machete to barriers to entry and friction in investing.

And this demand has led to the rise of huge financial media outfits and personal finance gurus.

Kuch kuch history

Just to set some context on how things used to be before the rise of the modern-day personal finance industrial complex. It used to be that in the 80s-90, your broker used to be everything right from your best friend to your financial advisor. It’s just that he was your best friend selling you shitty stock tips, scammy insurance policies or costly mutual funds which 4-5% commissions. But then things changed, in the 80s in the US, brokerage commissions were deregulated, which meant that the market decided the brokerage. This gave birth to modern-day financial behemoths like Charles Schwab and TD Ameritrade (both now merged), E*trade which now manage trillions in retail assets in various capacities. This deregulation ended with brokerage going Zero in 2019.

The late 90s and early 2000s also gave birth to the asset management super giants – Vanguard, iShares, Schroders, Amundi, Allianz, Northern Trust etc. Vanguard and iShares alone today manager over $13 trillion in assets. This was also the time during which various regulations being formulated to regulate distributors and investment adviser (RIAs).

In India, Kothari Pioneer became the first private AMC in 1992, until then the show was run by UTI and banks like Canara, PNB, SBI etc. NSE became the first to offer electronic trading in 1994 and almost dealt a death blow to BSE. And in 2010, Zerodha introduced the concept of discount broking with a flat-fee model in India which has led to an intense pricing war since 2018 among the India brokerages. In 2013, SEBI notified the investment adviser (RIA) regulations and has been tinkering with them ever since. It recently made some big changes that might have killed individual RIAs.

But, Indian and US markets are more alike than different when it comes to the dominant financial intermediaries. Both the markets are dominated by insurance companies, banks and mutual fund distributors. RIAs are but a tiny part of the markets. As such, product have always been sold, scammed, shoved down the throats of gullible targets than sold right or bought.

The bullshitters

Coming back to the reason why I’m writing this longwinded post. Incentives make the world go round. To put it another way, where there’s demand, there’s supply. The ever increasing investor base and the internet have opened up a lot of business opportunities to build brands and businesses.

The thing about money is that 9 out of 10 people don’t know what they are doing. And the general human tendency of overconfidence means that these people don’t know or don’t want to accept the fact that they don’t know anything about money. This reminds of this legendary speech by Donal Rumsfeld:

And ignorance breeds experts and gurus. Take this lady for example. Her name is Suze Orman, and she calls herself a “Personal Finance Expert” 🙄She used to host a popular personal finance show on CNBC, and then she transformed into the Gwyneth Paltrow of finance (If you didn’t get this reference, Google the term Goop). She’s authored dozens of books, has a podcast and is now comfortably retired on a private island in the Bahamas.

Now, I didn’t know about this character until this beautiful timeless piece of advice blew up on the Twitter. I don’t know enough words in English to describe the wisdom, why don’t you click play.

Your entire world turned upside down right? Didn’t you mind just shatter?

Wait, I got more, here’s another seemingly good but stupid piece of advice 👇

Just utterly asinine advice. Shaming people money because they drink coffee? Why not take it a step further?

- Don’t use toothpaste, it’s like spitting Rs 9000 down a sink. A 100gm tube of Colgate classic costs Rs 52. Assuming that you use one tube a month and instead save that money at 7%, in 10 years, you would’ve saved Rs 9000. Instead, plant a neem tree and use the sticks.

- Don’t use a Deodorant, it’s like stinking up Rs 20597 under your armpits. A Nivea basic deodorant costs Rs 119. If you save that instead, you would’ve saved Rs 20597 in 10 years at 7%. Since you would’ve already planted a neem tree, you can rub the leaves on your armpits – good smell and anti-bacterial too. One tree, two uses.

- Don’t use soap, it’s like wiping Rs 4896 vigorously over your body. A bar of Lifebuoy classic is Rs 28, if you save that money instead, you would’ve saved Rs 4846 in 10 years at 7%. Since you already have planted a neem tree put those leaves in the bathwater along with some basis. Total ayurvedic germ buster gangsta move!

- Don’t use a mobile phone, it’s like talking away Rs 54713. A decent smartphone costs 10,000 and assuming a monthly bill of Rs 200, if you save both, you would’ve saved Rs 54713 at 7%. You can buy a pigeon for as little as Rs 500, if you buy a couple, you can use them as couriers. You get style points among your family members too.

- Don’t use underwear, it’s like wiping Rs 28750 with your ******* every day. A pack of 2 Jockey underwear costs Rs 300. If you save Rs 600 a year, you would’ve saved Rs 28750 at 7% in 10 years. Instead, you can buy 2 lungis for Rs 200 and make 15-20 makeshift loincloths. Kickass style too!

It’s not just this character, there are plenty of others. Take the case of Dave Ramsey, who runs a popular podcast and a radio show which is syndicated by over 500 radio stations. Even he readily dishes out some really terrible advice. He’s a built a cult following on top of his advice to people with debt. And his operation is a money-making machine. He runs a lead referral program which is rather brilliantly called “Endorsed Local Providers” for which he charges between $400-$900 a month. And not to mention the revenues he generates from the 10s of books he’s published, podcast ad revenues, media appearances and whatnot.

This program alone according to some estimates, pulls in anywhere between half a million to a million dollars.

Back of the envelope math shows that the former referral program and the current advertising program have been cash cows for Mr. Ramsey. If each of the 1,000 advisers in the program paid on the low end, $400 per month, that would translate into $400,000 of monthly revenue. If those same advisers paid on the high end, about $900, Mr. Ramsey’s business could see revenues of as much as $900,000 per month from adviser advertising.

Investment news

Wow, right now I’m thinking what the hell am I doing in my day job. If I could build a following by screaming and belittling debt-burdened millennials, build a following, start selling high commission products, even I can retire somewhere on a beach shack in Goa.

If you truly want to know what someone is doing something in the financial services industry, always look at their incentives.

Money shaming

But how do these gurus become so successful? Apart from the fact that that they prey on people’s anxieties about money, bullshitting about money is relatively easy because most people know very little about money. So, when someone who’s popular, famous or seems like an expert talks about money, people tend to listen to them. And more importantly, we also like being told, and it’s a pretty neat blame avoidance mechanism – it’s not us, it’s always someone else.

But one of the biggest reasons why these gurus become famous is because they make you feel like shit about your money choices. You’ll often notice that these gurus are loud, snarky, screaming, and blunt, like Jim Cramer, for example. Of course, this could all be an act or a carefully crafted persona to sell their garbage on TV. Remember, at the end of the day, this is self-serving entertainment masquerading as generous advice.

All this screaming and shouting is not for everyone:

I’m stressed about money and looking for answers. But instead of solutions, I’m called “stupid” for making an incredibly common money choice. Like running up a credit card balance, borrowing for college, eating out “too often.” In all of this personal finance advice, I’d just hear judgments: immature, ignorant, lazy, poor self-control, or simply “not wanting it” enough. And maybe it works for some people. But for me, the financial tough love approach can be downright dangerous.

Take the coffee example, I drink 5-10 cups of coffee outside, and when I first read that tweet, the thought of I am indeed pissing away Rs 50 to Rs 100 a day cross my mind. This is called money shaming, and it’s quite scarring. If you shame someone for taking on debt or using a credit card, of course, they’ll feel terrible. And this is a brilliant way to come out superior while belittling these commoners just because these people tend to have big platforms. Because they have a large platform, people listening to these gurus tend to place implicit trust in them and consider whatever stupid advice they dole out as gospel.

And money shaming is pervasive, look at this for example. A wedding is probably a once in a lifetime experience. Is it wrong to spend a little extra? Of course, if you take on high-interest debt, then it’s a terrible idea. But if you can afford to without raiding your retirement savings, then why the hell not? You don’t have to get married under a flyover, steal flowers from your neighbour and use a white bed sheet for a wedding dress and distribute Vada Pav as lunch!

Living life constantly looking for ways to save every nickel and dime is a horrible way to live. That stress and anxiety will probably knock off a few years of your lifespan or worse yet, give you a heart attack. Sure, you need to save a good chunk of your income, doesn’t mean you have to be miserable after you’ve saved. This is probably best embodied by The FIRE (Financial Independence, Retire Early) movement, which has become all the rage. At its core, the idea is to save the maximum you can by being frugal so that you can retire in your 30s or 40s.

But, there are FIRE adherents who take this to the extreme. Here’s a disturbing example where a couple took frugality to the extreme:

Our extremely frugal lifestyle took shape by cutting out almost everything we ever enjoyed. We cut our cable, slashed our mobile data plan, halted our habit of going out for dinner, and even put an end to our Sunday coffee dates. You name it, we cut it. But hey, we were going to retire early so we didn’t mind making necessary sacrifices to reach the FIRE finish line. But then something unexpected happened. As we watched our net worth climb higher and higher, we realized that our happiness level seemed to be in free fall.

And this FIRE movement is again a brilliant example of money shaming and snake oil salesmen and talking heads. There are millions of blogs and podcasts, some good but some really terrible which dish out harmful advice that just make people more anxious, which inevitably ends up having knock-on effects on your health. The people peddling this garbage make some good money from ads and other avenues. But you get the gift of being absolutely miserable and probably making others around you miserable for listening to those quacks. Is this worth it? Hell no, if you ask me, moderation and balance in all things.

These people don’t know shit, and they’re here to make commissions from products and from ads on their blogs and video. At this point I have to tell, I don’t make shit writing these long rants. 😛

Live a little!

Don’t get me wrong, I agree with the core premise of FIRE, that is to save as much as you can by being reasonably frugal. But living like a caveman by forgoing basics and being miserable all the time? What the hell! I’m not judging people who enjoy extreme frugality, if you want to wear a loincloth and retreat to a forest, by all means, let it loose and enjoy your life. But how many such people do you think exist?

You don’t have to forego coffees, comfortable underwear, occasional vacations, comfortable clothes etc. Of course, if you blow your savings on it, that’s stupidity, but you don’t have to be constantly anxious about what to buy and what not to. Drink a coffee at a simple hotel instead of Starbucks, buy cotton underwear instead of silk or satin, take a vacation to a low-key place instead of Paris and Rome. You can still live your life without having to constantly be anxious because you have benchmarked yourself to some bullshit standards set by a snake oil salesman.

This SNL parody does a brilliant job of mocking the absurdity of the advice dispensed by these gurus.

Look, if I am highlighting the bad, I’ll also highlight the good. Apparently, a lot of people also add that some of these personal finance gurus probably give a lot of good advice too, but my question is at what cost? Calling their advice biased would be an understatement. You don’t retire on the Bahamas by giving good advice, that you can be sure about.

I’m highlighting these US examples because they are readily accessible and read and followed by Indians too. But that doesn’t mean that this doesn’t happen in India. It’s amateurish, but we have our own share of gurus. It’s just that the personal finance scene in India is still fresh. Several popular self-professed personal finance experts making crores every year in mutual fund and insurance commissions by broadcasting terrible financial advice. Don’t get me wrong, commissions aren’t bad. Some of the best advisors today are distributors because being an RIA is a terribly undesirable and painful proposition.

But the thing about these guys and gals is that they are regularly featured on investing shows and write newspaper columns where they readily dish out advice like it’s eating popcorn. This amazes me. These people are making a mockery of financial advice. Think about it, how the hell can you go on a TV Show, talk to some random caller and make investment recommendations without understanding his or her life circumstances? It’s a joke! Not just this, every day, tens of investing columns are published doing the exact same thing. How can you give random advice? Who’s responsible if something goes wrong? In what capacity are these people giving personalized individual advice? Is adding a disclaimer and placing the onus on the investor absolve these platforms of their culpability? This is Financial Wankery at its best.

Coming back to the point about commissions, when you build a business on the back of such things and make money, that’s wrong! I’ve no doubt they might be competent financial folks but dishing out advice in public without a shred of responsibility, that’s morally incorrect. Since these gurus love using the doctor analogy, dishing out personal finance advice on TV and newspaper columns is just like a doctor advising patients on TV. That advice has as much chance of working out as a mosquito surviving after being trapped in underwear made from a lungi for one night. What if someone who is living paycheck to a paycheck and is the sole breadwinner of a family acts on public advice and things go south? This is 90% of all Indians by the way. Not that investors are innocent, their idiocy is almost always responsible for their terrible financial outcomes.

Preachy bullshit!

Do you know the irony of this whole mess? These guys are engaged in this shenanigans while constantly chanting that personal finance is personal and virtue signalling to the fullest. This probably has to be the most bastardized phrases in finance probably next only to “investing is easy but not simple”. But they take every chance to broadcast impersonal advice to anyone who is listening and feeling anxious about money. When anxiety meets a solution, guess what happens? Gurus and experts are born, and they will get their pound of flesh either directly or indirectly.

Coming back the internet, it has truly decentralized the ability for anyone to broadcast their voice and build a following. Ability to create blogs, vlogs, podcasts, live streams, it’s all free. But this on its own isn’t enough. All these things are like dry tinder but you still need a spark. And most often than not, that spark is the traditional financial media.

The thing about financial services is that, for all the bullshit about digital transformation etc, it’s still an industry that works on trust. That cannot be abstracted away until Blockchain tech is our lord and saviour. So, it’s not just enough for snake oil salesmen to peddle their horrible financial advice everywhere. This can only give them a limited number of weak and anxious minds to prey on. You need credibility, and for better or worse after all, that has happened, traditional financial media still enjoys some trust, I don’t know why but it does. But it’s slowly but surely fading away.

Now you have a perfect situation where demand and supply meet. You have the gurus, the experts, and the pundits who need a big platform and on the other side you have the hollowed out and decaying media outlets who need as much content as possible to run ads against and make money regardless of the quality of that content. And ta-da, you have all these financial advice programs where a mockery is made of the profession of financial advice.

Oh come on, they give good advice too!

At this point, you might be thinking all these gurus on these channels can’t be all bad, they give good advice too. But my questions is, are they qualified or allowed to? If a distributor who can only provide advice incidental to the product he is selling and gives advice specific individual advice publicly, how is that even legal? If an RIA who has to mandatorily do risk profiling before he advises an investors broadcasts, provide specific advice to an investor how is that legal? Forget legal, is that even morally and ethically right? Ok, let’s for a second assume that this open broadcast of financial advice is ok, which it is not. But let’s assume for a second it is, who is responsible for the advice if something goes wrong? To be fair, there are some bloggers who exercise an insane amount of caution and collect a lot of context before they give specific advice, but these people are extremely rare.

To be an RIA, you need to have a networth and minimum educational qualifications, you need to do risk profiling, audits, maintain records of client interactions and so on before you give advice. But if you are popular on social media, you can just go on a TV channel and start advising without having to deal with any regulations? In which fricking universe does this make sense?

Sure, I’m sympathetic to all the arguments that people also help others, promote financial literacy and all that. But do you honestly believe the damage that they are doing outweighs the supposed benefits they provide? It’s not just these gurus, and it’s also all these AMC heads, CIOs etc. These people are manufacturers, and they should stick to that. I get these people talking about stocks, industries and sectors or general things, but giving pointed and specific advice to investors about the type of fund to buy, insurance policy, etc that’s just unethical.

But think about why people listen to this generic bullshit. There’s this old saying about fund managers on Wall Street – “Nobody gets fired for buying IBM”. Translated to the Indian context “Nobody gets fired for buying HDFC Bank or Reliance” because these are the bluest of blue-chip stocks and the odds of you going spectacularly wrong are less. It’s the same with these snake oil salesmen, as long as you make enough sense, you can build a million-dollar media empire by spewing nonsense and ruining the lives of people.

At this point in this long piece, it might have skipped your mind. The one common thread across all these shenanigans, the reason why these shenanigans works are because people are anxious about money and they are susceptible to bullshit. And these people peddling dangerous advice just prey on these anxieties and the sweet part, they get to make money at it. Can’t get easier than that can it.

Real life is infinitely complicated and messy

When you’ve hit the ovarian lottery and are born rich, talking out of your ass about financial advice is quite easy. But when you walk amongst the common people, you’ll realize that’s maybe 10-20% of India or even less.

One of the most common personal finance mantras everybody shoves down your throat is to start saving early. They also throw the example of how Warren Buffet started investing at a late age of 11 for good measure. It doesn’t end there, and if these gurus find out that you didn’t start saving early by 18-20, they’ll look at you with scorn and disgust. They’ll make feel like shit like you had never before in your life. It doesn’t matter if you can save, your complicated circumstances don’t matter, your commitments be damned, you must save early, or you are doomed in life. You always have to compound, even when you are in the toilet. Compound first, go potty later!

This is such utter horseshit. The ability to invest early when you live in a relatively developing country like India is a mega luxury that most don’t have. When you are in your 20s, if you have enough disposable income to save, you’ve hit the lottery. But this, in my view, is probably 10-20% of the Indian youth. Only a small cream of the crop, due to their own talents and a generous dose of luck end up in high paying jobs and can afford to save early.

The remaining people live in real India. And that means low paying jobs or worse yet, unemployment and then all the commitments that come with the privilege of being a middle-class Indian kid. Again, these gurus would tell no matter the circumstances, you can always save something. Maybe, maybe not. Let me tell you an example of a childhood friend of mine, who wouldn’t make his first investment until his late 20s. In his early 20s, he was stuck in a dead-end job, a single-digit salary which was less than the rent he had pay. He also had to take care of his family debt, food, clothing and so on. And no he wasn’t an outlier, half of my classmates lived some version of this life. Starting a SIP was a luxury none of them could afford. They were busy dealing with real life. This isn’t a sob story, this is most of India.

Moreover, for the vast majority of people, the only real asset they have in their 20s is their human capital. This is the age when they have to invest in themselves so that they can enjoy the pay-offs later if they’re lucky. Making people feel like shit for not starting saving early exposes an annoying lack of appreciation of real-world circumstances.

You know what’s the mega tragedy, you have to deal with if you don’t start saving early? You just have to save more later in your life – big fucking deal! To be honest, it doesn’t make that big of a difference because there are far bigger factors which have a far bigger impact on your terminal wealth.

In fact, while in the early years the results are dominated by contributions – the growth doesn’t amount to much yet when there’s hardly any money in the account in the first place – by the later years, returns are the driver for almost all of the increases in the account balance as it drives towards the final goal. In other words, while there’s a benefit to starting early to enjoy the benefits of compounding growth, it actually makes the outcome remarkably reliant on returns in the final years; shortfalls towards the end simply cannot be made up with new contributions alone.

Micheal Kitces

If you are reading this in your early 20s and are feeling like shit because you aren’t able to save, relax. If you have enough income to save and you aren’t saving, that’s stupid but otherwise, relax. Build your skill set so that you have a bigger pay-off later in your career and you can save more. Untangling your financial life is just as important as saving. You can just cut corners and save, but being stressed and anxious all the time and not worth it.

The other ass backward advice these people generously dish is never to take debt. Again, no issues with the advice. But how many people take debt just because they are bored and want some enjoyment in life? I’m sure these types must exist, but a vast majority of Indians are indebted because of their circumstances, not because they like taking on debt because they’re bored. The difference between whether their sons or daughters graduate or not is a 30%pa loan from a moneylender, a student loan or worse yet credit card withdrawals. In the case of my friend, for a good chunk of his 20s, debt was also the difference between a full stomach and an empty stomach.

Now it sounds like I’m bringing up a lot of sob stories to make my point. My response would be to get off your little bubbles and walk on the streets for a day.

The other problem with this no debt mantra is, it’s quite easy to give this advice when you have a rich father or a big bank balance. But for a vast majority of Indian people, jobs are hard to come by, even if they do get a job, it’s most likely a pretty low paying one. And with the salary they get, they have to pay off their loans, pay rents, put food on the table and so on. These gurus would blame these people for their circumstances, but just like income inequality, there’s an opportunity inequality in the world too. Not everybody can pull themselves by their bootstraps. Real-life, for a vast majority of Indians, is incredibly messy.

By the 5th of every month after most Indian kids get their salary, the only thing they can probably afford is an underwear, that too if it’s only on sale on Myntra, forget a SIP.

The problem with generic advice is that people dishing it out have no idea what they are talking about.

If this is the reality, I wonder to whom is this advice of “start saving early” meant for because it isn’t for a vast majority of Indians.

Personal finance ain’t just personal, it’s nightmarishly complex

Investing is simple, but not easy.

Warren Buffett

We’ve all been sold a lot of bullshit on the back of this Buffett quote, and I’m pretty sure it’s been taken out of context. We hear things like keep simple and other simplistic bullshit. But nothing about personal finance is easy; it’s probably one of the hardest things you do in life. The sheer number of things you need to get right and the amount of luck you need is mind-boggling, as with most things in life. When people say, keep it simple, I wonder what exactly is it that I should keep simple!

Most of these experts live in a dreamland that personal finance is all about cutting debt and saving more. But that’s just tiny part of it. The only people who can afford keep it simple are the rich and well off. For the real people who live in the real world with real commitments, none of this shit works. For most of the personal finance experts and gurus, it starts with choosing a mutual fund or a low-cost fund. But if probably 50% of young Indians don’t have enough money to invest, and the remaining are probably stuck in dead-end jobs with weak prospects, what do they do with the BS advice that they should invest in an index fund?

I might be wrong, but Jon Stewart in one his videos said: “simplistic solutions to complicated problems” or something to the effect. Nothing describes the personal finance industrial complex than this. This industry is feeding off the weak and the vulnerable by churning our generic oversimplified garbage content at an industrial scale.

Every single goddamn thing about personal finance is complex. Which is why you need human advisors and technology won’t disrupt then until we have Artificial Intelligence as we saw in iRobot. Until and unless you understand the unique situations and circumstance of an individual, how the hell can you dole out advice? To give you a simple example of a complicated question, what if a person has some money to invest every month but has credit card debt at 40%PA and is on the verge of getting a divorce and will end up paying alimony?

An average middle class Indian is usually stuck in a maze of complex situations and commitments, I’m speaking from experience. Simplistic garbage advice designed to push products or build personal brands so that they can make money off you, that’s utterly disgusting.

And the thing is, Indians don’t have access to quality and affordable financial advice, even if we assumed that they want to figure out their situations. This is why mis-selling is rampant, and people are sold all sorts of garbage by banks, distributors, insurance salesmen, scammy personal finance gurus, Twitter experts and so on. Although some amount of mis-selling is needed to bring about financial inclusion, the egregious mis-selling at any cost, that’s running people. But that’s the only advice most Indians have access to.

The only real choice for most people is DIY – make mistakes, learn and figure it out. And in recent years, a cottage industry has also developed, and their whole shtick is to showcase their smarts by looking down on DIY investors. Reminds me of those 3rd standard shenanigans.

All the gyanis, distributors and advisors scoffing at DIY investors, these are the very people that will be out of business in a few years. When their entire branding is predicated on projecting an air superiority of know it all…ness, imagine the quality of the advice they would be giving. These are people detached from reality with no real understanding of just how complicated the lives of investors are. The fact that they are even in business is shocking.

The personal finance call-in shows, newspaper columns etc are the worst thing to have happened to investors since LIC uncles.

It’s broken!

It might sound like hyperbole but the modern financial services industry lost it’s way and sold it’s sold to the highest margin a long time ago. It’s fundamentally broken and isn’t working for low-income investors. Do you know what the irony is? It’s working even badly for rich people. From red carpet financial services firms like Goldman, Morgan Stanley to elite PMS’, AIFs, Hedge funds, rich people lose more money in fees than they’ll even make in returns even they stayed invested for 2-3 centuries. These firms have made shoving costly and complex and risky structured products down rich peoples silk underwear and extracting high fees an art form.

And it doesn’t work for people with no money. When the premise of an industry, with just a few exceptions, is predicated upon extracting as much rent as possible while screwing over the masses, how do you expect the investors to place their trust in them?

And sadly for investors, the financial regulators around the world haven’t been able to keep up with the evolution of the markets, the actors, intermediaries, financial media and financial services itself. Investors getting screwed over every day from shady advisors, distributors, insurance salesman, brokers, and other snake oil salesman have very little recourse today. The recent scams in Karvy, Anugrah, BMA wealth are a case in point. And I had written more about all the different ways in which investors get screwed over here. This isn’t a uniquely Indian phenomenon either. The number of enforcement actions that SEC, the US financial regulator bought in are at a 6-year low.

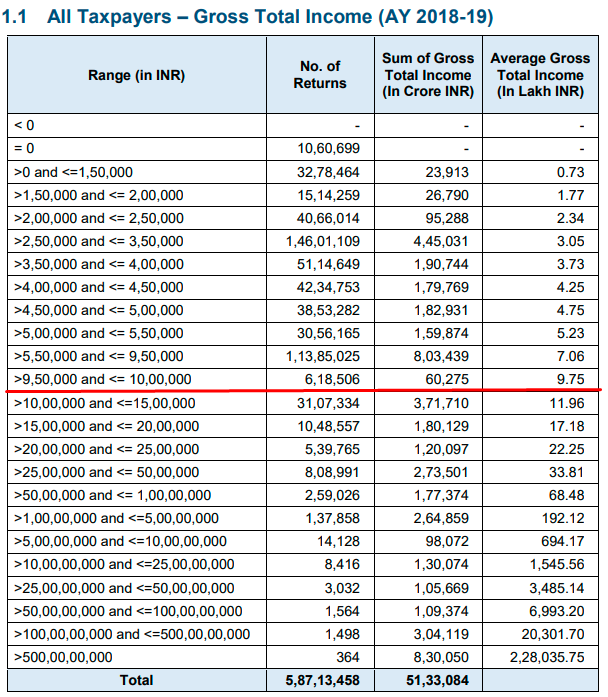

All the advice, all the fee models, they are barely working for the people who are investing, and there aren’t a lot of those. To begin with, there are just 5.9 crore taxpayers in India, our of which only 59 lakh taxpayers filed returns above Rs 10 lakhs.

There are 2.1 crore unique mutual fund investors in India, that’s it. You might argue that these IT numbers might not be representative and that a lot of people don’t file etc, but that’s a separate argument. We don’t have a huge population that can invest.

The existing ecosystem of advisors, distributors AMCs are just milking this tiny audience. There’s a reason why the %AUM fee model is a dominant one across modern financial services. One – it’s easy to collect and reduces the friction in payments. But the other major advantage of this fee model is that incredibly lucrative, larger the account size, higher the yield, which means that advisors and distributors naturally look for clients with larger account sizes. It doesn’t work for investors who don’t have a lot to invest. It makes no sense for someone to pay 1% commission if he can just save 10,000 a year. For a young investor starting out, his biggest asset is his human capital, a %AUM model makes no sense.

This is where alternative fee models like flat-fee, hourly, time-based, subscription pricing etc come in. But in India, we hardly have about 50-100 odd flat-fee RIAs. The other models are pretty much non-existent. And the result, investors who can’t save a lot are at the mercy of unscrupulous banks RMS, insurance salesmen and all sorts of other Ponzi schemes and scams.

Of course, you could have a purely rational justification that if serving someone isn’t worth the money, they won’t be served. But is this what it has come to? Is this how we should look at this sad state of mess? What then becomes of financial inclusion? If the incentives aren’t realigned, the remaining 10-20 crore Indians who can afford to invest at least something will never invest in financial assets. It will just be gold, FDs, chit funds, real estate, and emu farms.

The existing system is failing them, and the blame lies on all the people involved from the regulators to the AMCs to the intermediaries. Of course, it’s easy to complain, be sanctimonious. But aligning incentives to serve investor with small accounts is easier said than done, which is why the recent RIA regulations by SEBI are so regressive. No one in their right minds will now think of becoming RIAs, meaning the number of fee-only advisors will remain in the low double digits. The other issue is that collecting fees and managing portfolios, given that you cannot execute on behalf of investors is a nightmare. Without these things, advisors can’t be easily compensated and ensure that the advice they are providing is being implemented by the investor. Of course, there are a lot of reasons why this friction exists, but if it doesn’t go away, financial inclusion will be like that hymn we chant every day when we pray. We can keep doing it, but it’d be pointless.

To the investors

At the risk of giving generalized advice against which I just ranted, the only way you can avoid this doom loop is if you get your shit together by learning how to manage your finance. Make no mistake, it’s not easy, not simple, like with all things in life it’s incredibly hard. But ultimately, it’s your money and you are responsible. But the good thing today is that we are living in a golden age of information. Quality content about money is at your fingertips. For example, I have immensely learnt from blogs like Freefincal, Stockviz, Factor Investor, Varsity, Freefloat, Portfolio Yoga, Peepal Cap, CapitalMind among others. Khan Academy and other MOOC sites have 100s of free courses on money management.

At some point, you have to take responsibility for your own money. The easy advice I used to give all these days is to find a good advisor, but that’s easier said than done. You have no choice but to take responsibility for your own shit.

I find your blogs very interesting and I like your sarcasm as well. Would love to connect with you.

Yes difficult to become a Financial expert but be Personal Finance literate to avoid being scammed once too many a time, the desire to being a Financial expert will next follow

Good Rant. Took me 3 hours to read it.

Thanks for it.

Your next name change on twitter should be ” A Bull In China Shop. ”

Kick Them All.

Good article. But the rant is similar to Rahul Gandhi abusing Modi. No real solution offered. We all know the problems and the solution cannot be everyone becoming a Financial expert.

You should read all articles for the solutions… Best solution is Indexing. Nothing can beat it in the long term. Period.

Interesting article indeed. I wish there a time estimate were given at the beginning – took quite a while to read.

I like the advice to the investors – take charge of your personal finances. Fair enough.

But what do you expect the financial services or the wealth management industry to do? You want personalized advice to be given to a customer investing just ₹10,000 by a Harvard grad for a price of less than 100 rupees. Seriously? Unless you can get unlimited VC funding for all AMCs and financial advisors, that’s not going to happen.

Technology is the only possible way to solve this for masses but a truly personalized financial advice will continue to remain a dream for most Indians. And it’s not the financial services industry but pure economics to blame.

Also just a technical point, AUM based pricing model Infact works better for small investors – an investor doing 10,000 pays effectively only 100 rupees per annum. Is that a lot to pay for basic convenience, let alone financial advice?

Thank you! Tum bahut mast kaam karta he 🙂