Updates

The cabinet has approved the launch of the Bharat Bond ETF

Unit size: Rs 1000 for the ETF. NAV of the FOF will be Rs. 10 during the NFO period but Edelweiss has yet announce the minimums.

Expense ratio: 0.0005 percent

NFO Date: 12th December to 20th December

The NFO of the Bharat Bond ETF (PSU Debt ETF) is set to open in December, probably 2 to 3 week. I am hearing December 19th as the NFO close date. Will keep the post updated. So, I was assuming that the AMC would launch multiple series for each year, but that’s not the case. There will be 2 series – 2023 and 2030. Essentially 2 ETFs, that will expire in the year 2023 and 2030. 3 years because of the indexation benefit. But still this is a really cool structure because of the defined maturity, you clearly know what the duration risk is.

Last year, in the budget, the govt had announced that along with CPSE and Bharat 22 ETFs, it wanted to raise money through a debt ETF. Post the bidding, Edelweiss Asset Management won the mandate to launch the debt ETF. We finally have details on how the ETF will be structured, and it’s quite interesting!

So, I know a guy who knows a guy, who knows a guy in Edelweiss who knows about the workings of the proposed “Bharat Bond ETF.” I saw the product presentation and looks like, Edelweiss is using the target maturity ETF structure. But note, all these details are subject to change, and the AMC hasn’t yet filed the draft with SEBI, as far as I know.

By the way, this isn’t the first debt ETF to be launched. We already have a few of GILT (G-Sec) ETFs and Liquid ETFs. Although, the Liquid ETFs are well…liquid, the Gilt ETFs aren’t.

How dis target maturity ETF work?

A target maturity ETF is similar to a fixed maturity plan (FMP). Each ETF will have a defined maturity, say, for example, 2030 and will hold bonds with similar maturity dates. Unlike debt mutual funds, where a fund manager may churn the holdings, these target maturity ETFs will hold the bonds until maturity. Upon maturity, the money will be paid back to investors. All interest payments, can either be distributed to the investor or reinvested. In this case, coupons are stated to be reinvested.

For each maturity, an index will be created, and that particular target maturity ETF will track the index. Every time an ETF matures or approaches a maturity date, the AMC will keep launching newer ETFs to replace them.

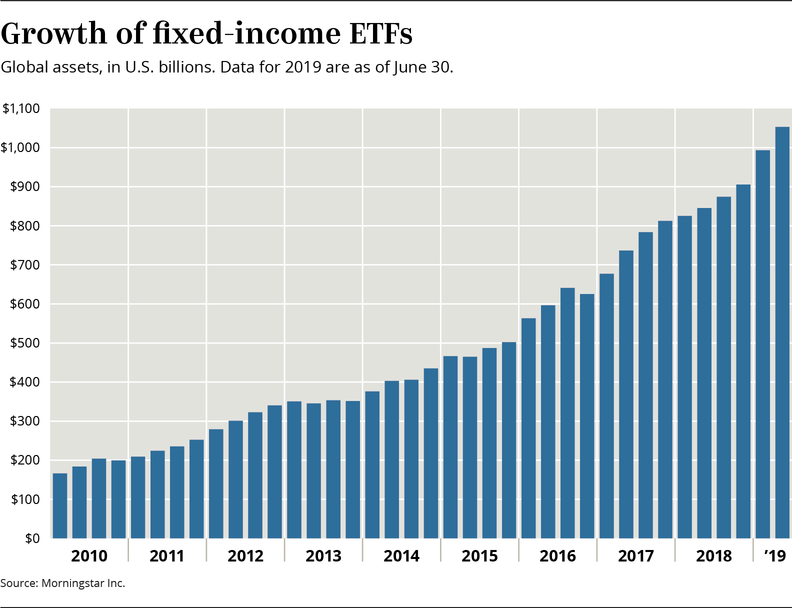

Even in the US, these target maturity ETFs haven’t really gained popularity. Combined, these ETFs had $20 billion in assets. Invesco BulletShares and Blackrock iShares are the two biggest issuers in this space. Bond ETFs as a whole held over $1 trillion in assets.

What bonds will the ETF hold?

The ETF will only hold bonds issued by Central Public Sector Enterprises (CPSEs) with credit ratings of AAA. Each bond issuer will have a weight cap of 20% in the index to reduce concentration risk.

Will these ETFs be liquid enough?

Well, the govt will market the shit out of these ETFs to retail investors. So, it would probably be fair to say that they won’t be severely illiquid. Afterall, CPSE ETF and Bharat 22 ETFs are very liquid. Also, Edelweiss will be launching Fund Of Funds (FOF) for the ETFs, which will aid liquidity. Why you ask? Because ETFs require demat a/cs and not many people in India have them. FOFs were launched for CPSE ETF and Bharat 22 ETF as well.

Are these ETFs safe?

Well, these ETFs will only hold bonds by PSU entities. And moreover, PSU entities have something of an implicit sovereign guarantee. Meaning, the govt doesn’t explicitly say that we guarantee the debt of PSU companies, but if shit hits the fan, they will most often than not step in and make investors whole.

What will be the expense ratio of the ETF?

When it was announced that Edelweiss won the mandate for launching the ETF, few outlets reported that it proposed an expense ratio of 0.0005%. I have my doubts, and it’s still early to speculate on this. Better to wait for more details to emerge.

But this ETF will likely be an NGO product. The expense ratio of both CPSE ETF and Bharat 22 ETF is 0.01%. Also, given that there will hardly be any management given that the ETF will most likely be held to maturity by most investors, it would be fair to speculate the ETF will be cheap.

What’s the taxation like for the ETF?

If the ETF is sold before 3 years will be treated as short term and Short term capital gains (STCG) as per your income slab will be applicable. Long term capital gains (LTCG) of 20% with indexation benefit post 3 years.

Will the issue be successful?

Absolutely! We have already seen how savvy the govt has been at dumping its useless PSU holdings through Bharat 22 and CPSE ETFs. Govt had raised Rs 50,000 crores from all the tranches of CPSE ETF and Rs 22,900 crores from Bharat 22 ETF issues. There is no indication yet, as to the fundraising target for the debt ETF.

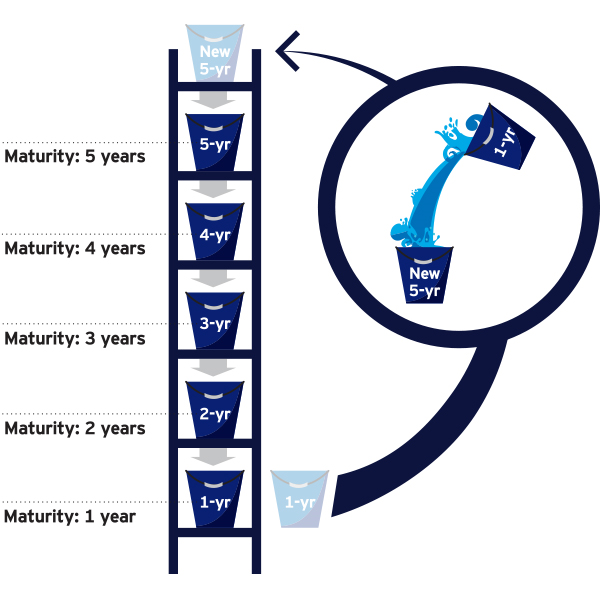

Also, the cool thing about these ETFs is that they will make the construction of bond ladders very easy. A bond ladder is a strategy where you build a portfolio of bonds with staggered maturities – say 1-5 years. Every year a bond expires, you reinvest it in the longest duration bond, like the illustration shows.

But constructing a ladder with individual bonds is very difficult. The advantage of a bond ladder is that it helps you reduce the interest rate and reinvestment risks. Here’s a really nice explainer on laddering.

I will keep my tongue peeled for more details. But this is a very exciting development for ETFs as a whole. Although these are very very early days for ETFs, volumes have been growing. The launch of this ETF will only make them more popular.

Also, check out this explainer on defined maturity ETFs by Invesco.