I’ve always been a bit smitten by the markets. I remember carrying a copy of Economic Times to school. I also very vividly remember buying the very first edition of Livemint when it launched in Bengaluru. In those days, I understood very little, but I was still curious though.

I remember asking my brother who used to trade to invest some of my pocket money in Reliance Natural Resources (RNRL) stock, not sure if anyone remembers it anymore. It was sort of an RCOM before RCOM.

It was the heyday of Anil Ambani and this was one scammy company in an otherwise long list of those. Anyway, I was lucky my brother was very forgetful.

The very first time I actually traded/invested was during the 2015’s, right in the middle of the Modi rally. Given my commerce background, I was helping a friend of mine to trade. It was one of those “I told you so” markets and everything was going up – junk and quality alike. WhatsApp and Telegram groups were abuzz with multi-baggers and the next Indian Apple’s and Microsoft’s. I’ll admit, I am a bit a guilty of trading those. It was a hit and miss kind of a phase.

It was a time when I was trying to do something on my own in life, rather unsuccessfully. So after a while, I had to quit and jump back into the world of gainful employment.

At this point of time, I was in my mid 20’s and had ZERO savings to my name. I, like many a folk, have the same regret of not starting to save early, but hey, mistakes right. But anyway, serendipitously for me, I ended up in a support desk in a financial services firm. It was another 2 years until I actually started saving, given that my personal circumstances weren’t leaving me with a surplus and I had a size zero paycheck.

In a couple of years, I caught a lucky break and got a chance to move to be part of a new team that was doing some exciting stuff. As I grew into the job, my financial situation improved considerably and I had some money to save.

My first investments were 2 SIPs in DSP Top 100 Equity Fund and

Mirae India Opportunities Fund, which later became Mirae India Equity Fund. Like you might have already guessed, these were recommended by a relative of mine, given that I knew next to nothing about mutual funds.

In retrospect, these turned out be rather poor choices and I’ll explain why. When I started investing in mutual funds, I knew nothing about how funds worked, the importance of costs, asset allocation or any of the other important things that an investor should know. I knew about indexing as much as I knew about quantum computing. The only decent choice I made during this phase was to invest in direct plans.

One thing that constantly amazes me is how the Internet has democratized information. Today you can pretty much learn anything under the sun from the history of royal food and feasting to molecular biology online and for free, as long you have the desire. Reminds of this quote by Naval Ravikant:

I wasn’t happy knowing that I was investing based on advice from strangers. I wanted to learn more about investing the right way, whatever that was and so began the Googling. Of all the resources out there, podcasts were an invaluable source of learning for me. I started listening to interviews of famous investors. But I had my Eureka moment when I heard some old interviews by Jack Bogle. Then I discovered the wisdom of Burton Malkiel and Charles Ellis and that was all the advice I ever needed 🙂 I’ll create a separate post with links to the resources that helped me in gaining the perspective I needed.

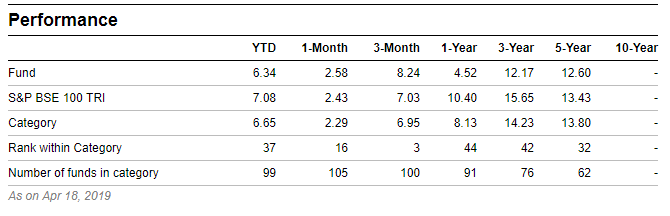

Then the creeping realization that I was plain dumb and stupid with my investing started to sink in. One fine day, I decided to look up the performance of DSP Top 100 Fund. I think every investor has a “what the actual fuck” moment and this was mine. This stupid fund had never beaten its benchmark.

And what was I playing for this stellar performance? 1.45%!! Yeah, that’s how fricking stupid I was. The Mirae India Equity Fund wasn’t as bad as this but, I got ripped off in another way. Although the way I got advice was bad, the fund wasn’t all that bad at first blush. It was a multi-cap fund and that seemed like a decent choice in a portfolio. Turns out, I was about to be made a fool of. This fund recently became a pure large-cap fund.

The justification the CEO gave for the move was this:

Isn’t that misleading? But anyway, that’s an argument for another time. By the time I had a rudimentary ability to analyze the funds that I was holding, I had understood my limitations as an investor pretty well. I was no stock picker and I was most certainly not a trader. I realized the best thing for me would be to continue investing in mutual funds.

Although I knew that indexing just made a lot of sense, I thought it was purely a phenomenon limited to the US. I was still under the assumption that Indian active funds, to some extent could still deliver some alpha.

During this passage of time, SEBI asked AMCs to use total return benchmarks and reclassified all the mutual fund scheme categories. What this meant was, the universe of stocks and bonds that funds could invest in was clearly defined. Large-cap funds, could now only invest in the top 100 stocks by market cap. This meant that large-cap funds could no longer slyly invest in midcaps to juice up returns. Yes, these sneaky lil shits used to do this.

So to sum up my mistakes:

- I got started with investing in all the wrong ways possible

- Chose instruments I didn’t understand

- No goals, no asset-allocation

- No idea about the importance of costs

And that’s when it hit me – it was time to give my portfolio a makeover. I didn’t take much for me to realize that my mostly large-cap oriented portfolio had to change. By this time, I had realized that picking good managers is easier said than done, in fact, it was the equivalent of picking a stock. There’s no doubt that Indian mutual funds had delivered alpha in the past but as regulations changed and as the markets matured, my bet was that passive investing would take off.

I recently redeemed both the Mirae and DSP funds and started investing into Nifty 50 and Nifty next 50 index funds. Now, I am not fully a passive investor yet. I continue to hold Mirae Tax Saver Fund and Parag Parikh Long Term Equity Fund. If I had a choice of an index ELSS fund, I wouldn’t have chosen the Mirae fund for sure. I will, however, continue to invest in the PPFAS fund because I like the philosophy of the fund house and the international geographical diversification also helps.

I’ve realized that I have as much chance of finding a good active fund as Abhishek Bachchan winning an Oscar. Of course, I want high returns and to grow rich, but I have to contend with reality. The reason I am almost fully passive is because I’m content with getting market returns. I also have a little active exposure in the hopes that I’ll get some kicker in returns.

I don’t want to run the risk of choosing managers, nor continue paying higher costs for shit performance. And that’s the story of my almost warm and tender embrace of index investing – the desire for that sweet luscious beta!

Thank you for your time and sharing knowledge. when you say index investing, what are the mutual fund names you ?

Bad start for your investment,if you had invested in kotak multicap and Mirae large,then your Philosophy would have been different beacz this funds have beaten it’s benchmark massively…

Wow, if only there was some way to predict that the fund would do well in the future.

Well Said!!

is the other post based on the resources from Charles Ellis and Burton Malkiel available?

Which post?

You have mentioned that you will create a separate post ..”Then I discovered the wisdom of Burton Malkiel and Charles Ellis and that was all the advice I ever needed I’ll create a separate post with links to the resources that helped me in gaining the perspective I needed”….so wanted to know if you can share the resources that helped you gain the perspective.

Ah, not yet. But we have the next edition of the indexheads.substack.com newsletter will include some good stuff by these legends.